click below to login to your secure account

By Tom Kozlik

Head of Public Policy and Municipal Strategy

Hilltop Securities Inc.

Investors struggled to find equilibrium throughout March. The Municipal Market Data (MMD) 10-year AAA municipal yield, the key benchmark for municipals, closed yesterday at 3.16%, and has risen 64 basis points since Feb. 27. The Bloomberg Municipal Bond Index closed yesterday at a 3.80% yield, up 51 basis points since Feb. 27. The 10-year U.S. Treasury closed yesterday at a 4.35%, a 41-basis point increase since the end of February.

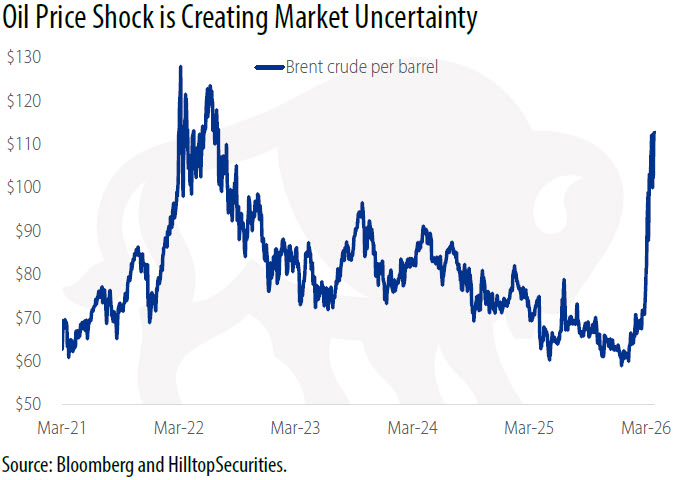

At the March Federal Reserve meeting, the FOMC left its target rate unchanged and emphasized patience, offering little indication that conditions for easing are close. At the same time, some market participants and observers now acknowledge that a rate increase cannot be ruled out. One of the most important indicators markets have watched this month is related to energy. Brent crude ranged from roughly $77 a barrel to as high as $113.

Investors are trying to infer and forecast at least three things simultaneously related to the conflict in the Middle East.

First, markets are trying to decipher the Trump administration’s actual intentions toward Iran. Second, how Iran is likely to retaliate, and whether that retaliation changes the energy market structurally rather than temporarily. Third, whether Brent crude remains high for long enough to turn a regional military conflict into a U.S. inflation (or recession) problem. That is why market sentiment has remained uncertain.

Treasury Secretary Scott Bessent did little to calm markets last Sunday when he said on Meet the Press that “sometimes you have to escalate to de-escalate.” Markets probably should have taken the Treasury Secretary’s’ words more literally. He was indicating that escalation is coming and that this conflict may not end quickly. Policy signals from Washington remain mixed, even as the Pentagon prepares to send 3,000 troops from the Army’s 82nd Airborne Division to the region.

For municipals, the immediate impact has been a rates shock. We are not yet at a point where a significant credit impact appears likely. However, the potential for either positive or negative credit effects grows the longer oil prices remain elevated. Tax‑exempt yields rising at the pace described above are not supportive for near‑term municipal prices, but they do improve near‑term conditions for buyers of new bonds. New capital is being paid more to step in, and buyers are being handed a better entry point than we have seen in months.

The supply and demand dynamic is always important in the municipal market. It matters even more now because demand has remained strong and consistent, while supply is elevated. If anything, demand has remained firm in part because investors continue to seek stability in their portfolios. In the first two months of 2026, investors largely sought strength in response to technology‑related developments. In March alone, nearly $4 billion has already flowed into municipal mutual funds per Lipper data, with another week to go. Year‑to‑date inflows now total just over $17 billion. At this point last year, flows were net positive but totaled just under $6 billion.

The comparison to the Bowles‑Simpson National Commission on Fiscal Responsibility and Reform is unavoidable. The 2010 commission also attempted to force a reckoning with long‑run fiscal imbalance. It did not produce immediate legislative action, but it did elevate deficit reduction and tax expenditures as central policy questions. That is why any new fiscal commission warrants close attention from municipal market participants. Increased scrutiny could place federal tax preferences under a brighter light, and the municipal bond tax exemption remains one of the largest and most visible preferences in the tax code.

Talk of a second reconciliation bill in 2026 has resurfaced, but it remains highly speculative. Its likelihood is constrained by the absence of a clear agenda, the lack of a viable legislative vehicle, and the realities of midterm‑year politics. While reconciliation always keeps the tax exemption theoretically in view, there is little evidence that Congress is organizing around a revenue‑driven effort that would put it back squarely in the crosshairs. The tax exemption is never fully off the board, but there is still little indication that curtailing it has become an active congressional priority in this moment.

Senator Joni Ernst’s Modernizing Agricultural and Manufacturing Bonds Act (MAMBA) proposal is far more concrete. It would modernize Industrial Development Bonds and Aggie Bonds, carries bipartisan support, and has earned broad backing from market participants. It is clearly supportive of the municipal bond market. Its challenge is not policy logic, but finding a legislative vehicle, and for now it remains credible and constructive, but not imminent.

Readers may view all of the HilltopSecurities Municipal Commentary here.

![]() As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or tom.kozlik@hilltopsecurities.com.

As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or tom.kozlik@hilltopsecurities.com.

The paper/commentary was prepared by HilltopSecurities (HTS). It is intended for informational purposes only and does not constitute legal or investment advice, nor is it an offer or a solicitation of an offer to buy or sell any investment or other specific product. Information provided in this paper was obtained from sources that are believed to be reliable; however, it is not guaranteed to be correct, complete, or current, and is not intended to imply or establish standards of care applicable to any attorney or advisor in any particular circumstances. The statements within constitute the views of HTS Public Finance as of the date of the document and may differ from the views of other divisions/departments of Hilltop Securities Inc. In addition, the views are subject to change without notice. This paper represents historical information only and is not an indication of future performance. This material has not been prepared in accordance with the guidelines or requirements to promote investment research, it is not a research report and is not intended as such. Sources available upon request.

Hilltop Securities Inc. is a registered broker-dealer, registered investment adviser and municipal advisor firm that does not provide tax or legal advice. HTS is a wholly owned subsidiary of Hilltop Holdings, Inc. (NYSE: HTH) located at 717 N. Harwood St., Suite 3400, Dallas, Texas 75201, (214) 859-1800, 833-4HILLTOP.