click below to login to your secure account

By Scott McIntyre, CFA

Co-Head of Investment Management

HilltopSecurities Asset Management

The U.S. economy entered 2026 with momentum appearing to slow, although business spending (driven by A.I. infrastructure investment) and consumer spending (bolstered by higher tax refunds) promised a first quarter bounce. Inflationary pressure eased early in the period, labor conditions continued to cool, and consumer confidence soured while consumer spending remained resilient. As the quarter progressed, the evolving U.S. military conflict with Iran drove crude oil prices sharply higher, abruptly rerouting the inflation outlook and reinforcing the Fed’s cautious monetary policy stance.

By quarter‑end, with the war in the Middle East escalating while entering its second month, inflation concerns completely dominated the news, and uncertainty drove market volatility to nauseating levels. Stocks fell and bond yields soared as expectations for near-term rate cuts faded away.

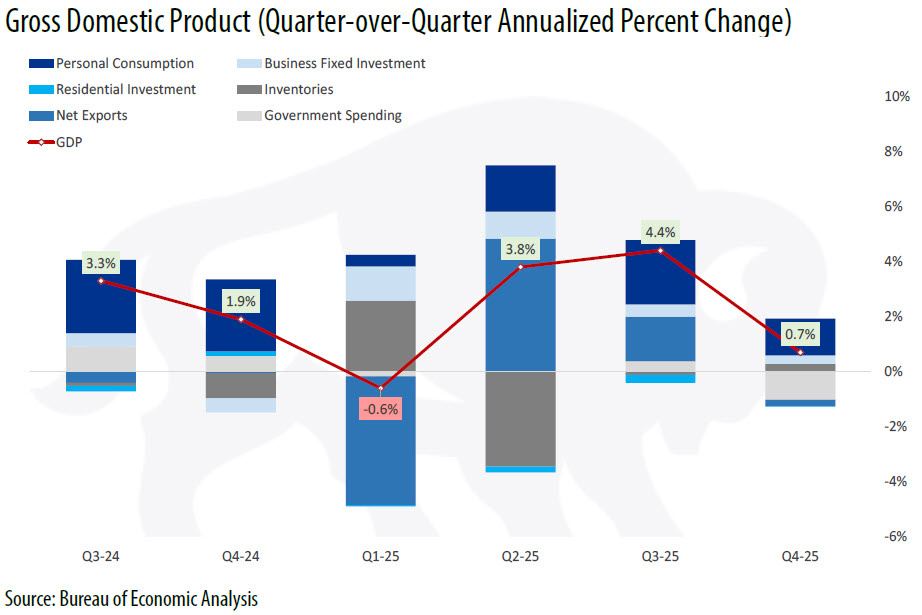

Headline GDP growth proved surprisingly tepid in the fourth quarter. The 45-day government shutdown extracted nearly a percentage point, and the +0.7% quarter-over-quarter annualized rate lowered full-year 2025 GDP growth to +2.1%, down from +2.8% in 2024 and +2.9% in 2023.

Because containing inflation is the sole mandate of the European Central Bank (ECB), policymakers across the pond may be forced to reduce consumer demand by raising interest rates. Given the already fragile economic conditions in the EU, this action could tip Europe into recession. In an emergency meeting on March 31, the European Commission urged member nations to encourage citizens to work from home, drive and fly less, and for EU countries to urgently roll out renewables, as it warned of a prolonged energy crisis as a result of the conflict in the Gulf (Politico).

U.S. stocks plunged in early trading this morning but have since rebounded on news that Iran is drafting a protocol with Oman to monitor traffic through the Strait. Bonds could have sold off this morning, anticipating the rise in inflation, but have staged a small rally in what is either a flight-to-quality or expectations that the domestic economy will be negatively impacted.

The markets are jittery, which suggests no real trend and a possibility that this commentary could be stale before the morning concludes.

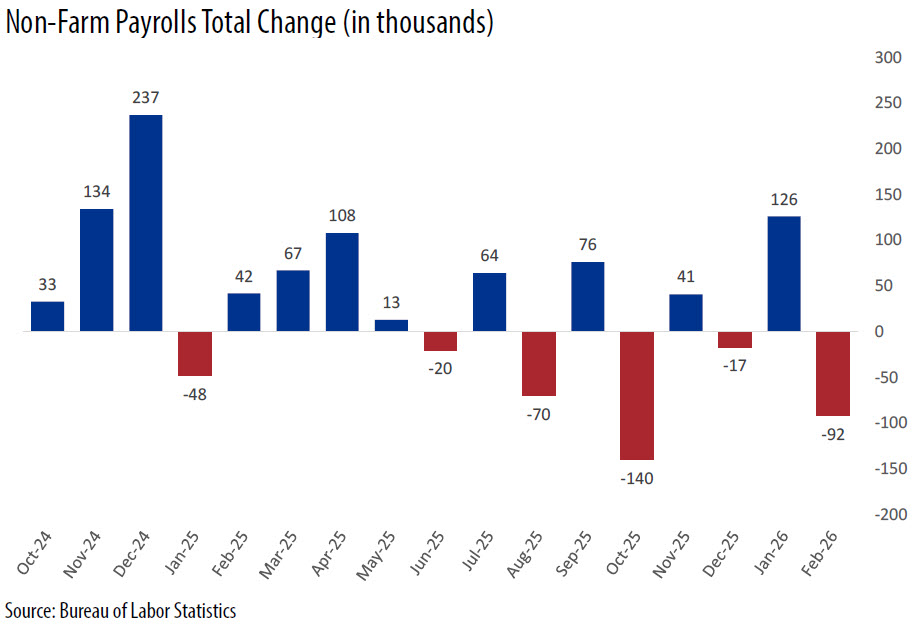

A slowing economy will typically produce fewer jobs, and this softer employment trend is already well-established. Labor growth has slowed significantly since last April, and a -92k drop in February nonfarm payrolls marked the fifth contraction over the past nine months. This has only happened a dozen times in the past 85 years with nearly all cases coinciding with or immediately preceding recession. In fact, there are no post‑WW2 examples where the economy dodged recession and re‑accelerated meaningfully after negative payrolls in five out of nine months. However, demographic shifts, recent immigration policy and rapid technological advances suggest this time may be different.

The unemployment rate reached a four-year high of 4.5% in November, before backtracking to 4.3% in January and 4.4% in February …although this is a bit misleading as the math has changed. The surge in retirement among baby boomers, which began about 15 years ago, has lowered the participation rate as retirees are still counted within the total population but no longer participate in the labor force.

In addition, net international migration dropped to 1.0 million in 2025 (San Francisco Fed), down from 2.6 million in 2024, while the Brookings Institute actually show negative net migration between -10,000 and -295,000. When population growth slows or turns negative, job creation typically slows as well, not because companies don’t want to hire, but because vacancies are harder to fill. At the same time, the unemployment rate remains deceptively low because the number of jobseekers has declined. Thus, the labor market feels worse than the BLS data implies.

One of the Fed’s two policy mandates is maintaining full employment. However, it’s unclear exactly what constitutes full employment these days, and even less clear that the Fed’s traditional monetary policy tools are capable of counterbalancing the negative forces weighing on the labor market. At the moment, it probably doesn’t matter as the Fed’s other mandate, stable inflation, is the more pressing issue.

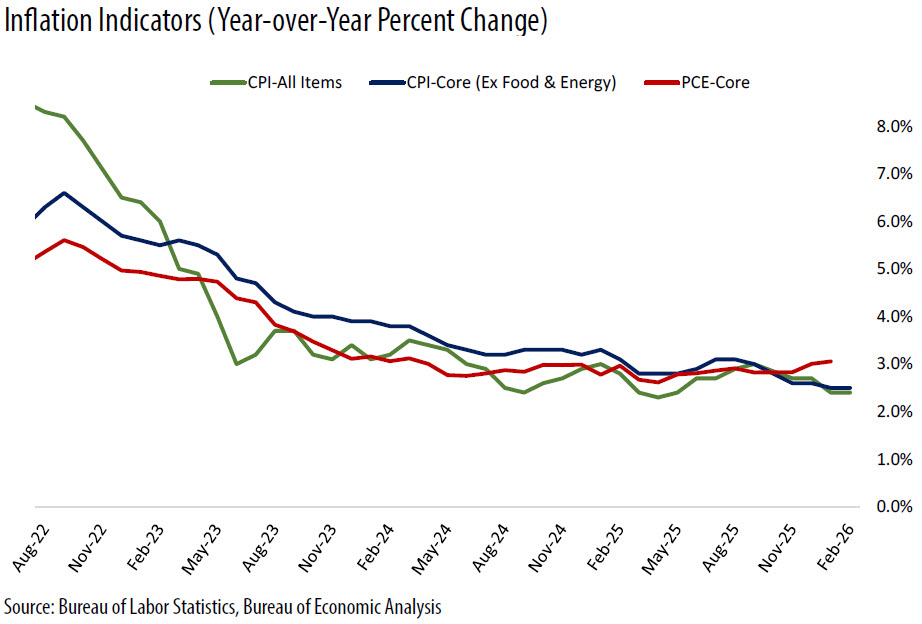

Inflation data early in the quarter mostly supported the disinflation narrative. Headline and core CPI both slowed in January, with shelter inflation continuing to decelerate and goods prices remaining subdued despite lingering tariff pressures. In February, overall CPI climbed +0.3% for the month and +2.4% year-over-year. Food and energy prices were both higher, but when these categories are excluded, core CPI rose just +0.2% in February and +2.5% year-over-year, equaling the lowest core pace since 2021.

Shelter costs are the primary reason why CPI has declined over the past three years, falling steadily from an annual rate of +7.5% in 2022, to +6.2% in 2023, to +4.6% in 2024 and +3.2% last year. This easing of housing costs continued into 2026, but overall progress on the Fed’s inflation objective was abruptly halted when war broke out at the end of February.

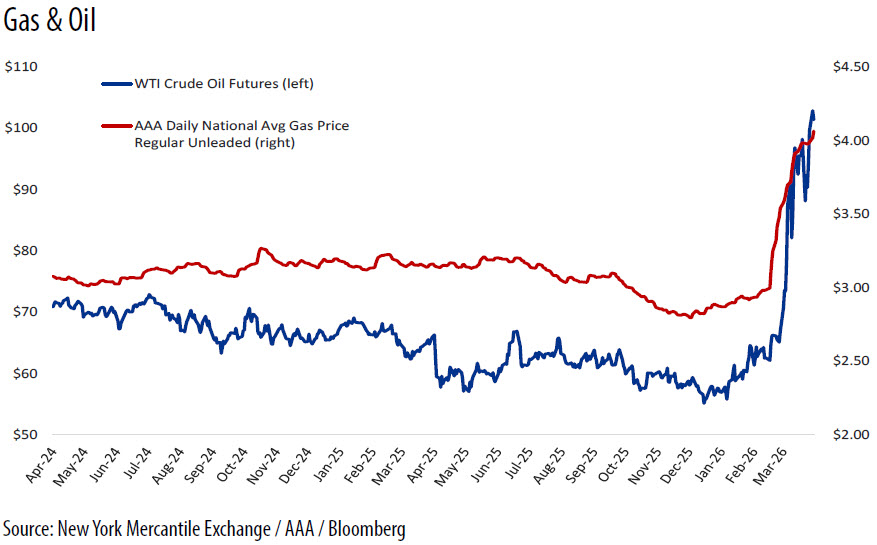

The escalating conflict in the Middle East sent WTI crude oil soaring above $100 per barrel, which had an immediate effect on gasoline prices. The national average for regular unleaded increased from just under $3 per gallon to $4 during the month, while the average price for diesel fuel climbed over fifty-percent and jet fuel close to sixty-percent.

Energy is a small component of CPI, but the month-over -month gain in March promises to be huge, reversing energy disinflation that drove earlier CPI prints. While history suggests the higher oil prices will have limited pass‑through to core inflation, if sustained, elevated energy costs can tighten financial conditions and weigh on real income growth.

CPI is front-page news and the most familiar inflation measure, but Fed officials focus on the core personal consumption expenditures (PCE) index, which at +3.1% in January was roughly a half point above CPI, a full point above the Fed’s target, and trending higher. The question is no longer whether inflation is falling, but how resilient any progress made so far will be to geopolitical supply shocks.

Consumer behavior in the first quarter reflected a widening gap between spending and sentiment. Nominal consumer spending continued to rise, driven primarily by services and supported by real wage gains. At the same time, consumer confidence wavered. In a March Harris–Guardian survey, 51% of Americans said the U.S. economy is getting worse, compared with just 20% who believe it is improving while a whopping 57% of Americans said they believe the U.S. economy is currently in a recession, despite official data showing continued (though admittedly fragile) economic growth.

The University of Michigan consumer sentiment survey had indicated the lowest current conditions reading in the history of the survey in December and the January Conference Board confidence reading was the lowest since 2014. The March University of Michigan survey showed Americans were increasingly concerned about gas prices, geopolitical risks and job security. Given the recent surge in pump prices, sentiment is unlikely to improve much, if any, in April.

For now, gloomy consumers are still spending. The risk is that elevated energy costs or a softer labor market could result in reduced spending in subsequent quarters.

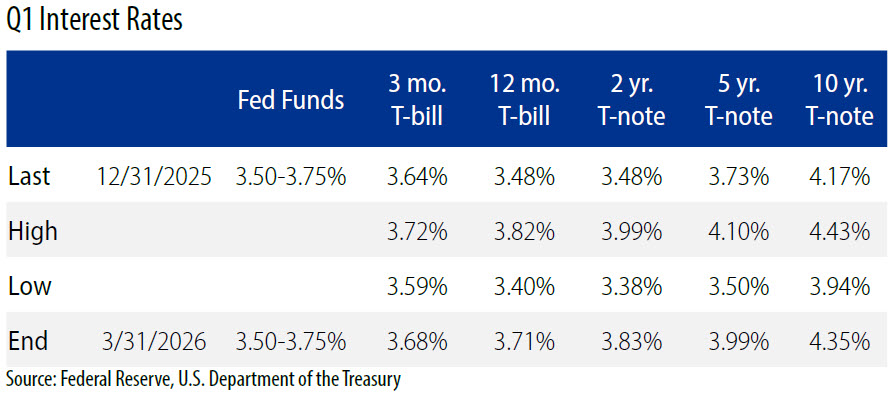

With one eye on an increasingly fragile labor market and the other on a deteriorating inflation outlook, Fed officials voted to hold the overnight target range steady at 3.50% to 3.75% at both the January and March FOMC meetings. The tone of the committee remained cautious and explicitly data‑dependent. Notably, the post-meeting official statement on March 18 acknowledged uncertainty related to developments in the Middle East, a rare reference to geopolitical risk in the normally paint-by-numbers summary. Policymakers emphasized that while oil price spikes alone would not prompt a policy response, persistently higher inflation expectations or deteriorating financial conditions were factors to be considered.

In the Fed’s first summary of economic projections (SEP) since December, committee members increased their 2026 GDP forecast from +2.3% to +2.4%, while core inflation was recalibrated upward from +2.5% to +2.7%. The unemployment forecast was unchanged, still expected to end the year at 4.4%, matching the rate in the February BLS report. Although there is clearly upside risk to inflation and downside risk to growth (and employment), it’s far too early for speculation. Given the rapidly shifting global landscape, the committee’s overly cautious SEP is probably meaningless.

The Fed is in a tight spot. Employment is soft enough to justify eventual easing, but the expectations for higher inflation argue for tightening. Geopolitics will influence both mandates, and the conflict in the Middle East has proven wildly unpredictable. For now, policymakers will simply wait.

Financial markets don’t respond well to uncertainty and are far less patient than the Fed. There were very few places for investors to ride out the storm.

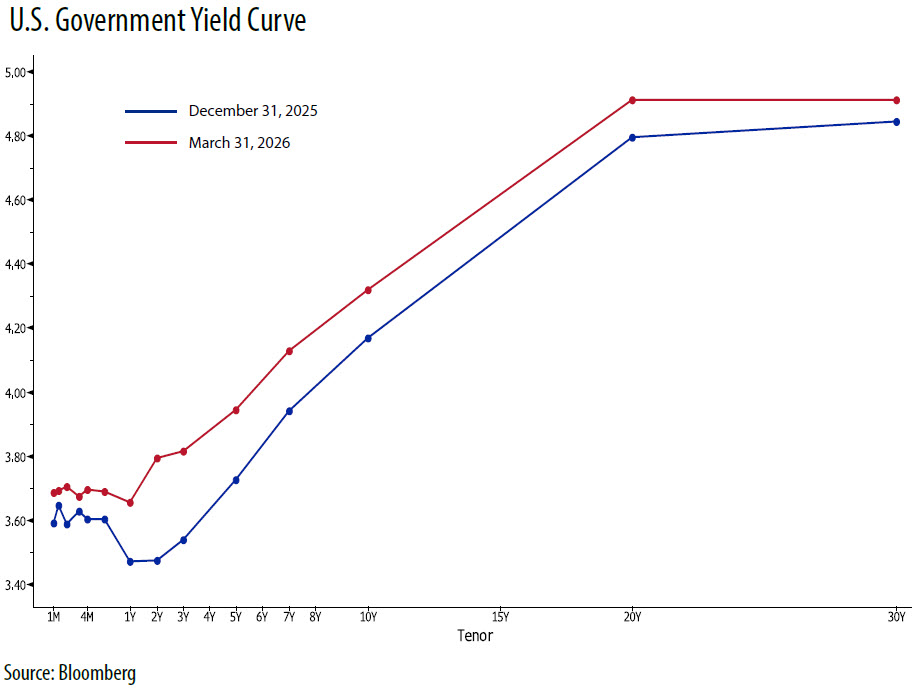

Short‑term bond yields were anchored by steady Fed policy, but longer‑term yields moved sharply higher in March, reflecting increased inflation risk, heavy issuance and geopolitical uncertainty. The 2-year Treasury note yield rose 42 basis points during the month while the 10-year yield climbed 38 bps, ending the quarter near an eight-month high.

It wasn’t just bonds that were clobbered. Virtually all major asset classes took a hit in March. Gold plunged -11% but still ended the quarter up +8.6%. Bitcoin eked out a tiny gain in March but shed more than -22% over the three-month period. The Nasdaq fell into correction territory in late March before staging a massive rally on the final day of the quarter. The two other major U.S. equity indexes followed a similar pattern, tumbling throughout March before clawing back a portion at quarter end. The Dow (-3.6%), Nasdaq (-7.1%) and S&P 500 (-4.0%) still experienced significant losses to start the year with the broad market S&P 500 delivering its weakest quarterly performance since 2022.

Whereas the economic effect of the war has been relatively muted for most Americans, effects are far worse across the pond. The European Union (EU) imports the majority of the oil and gas it consumes, and a meaningful share of this supply is tied to Middle Eastern production and shipping routes. In an emergency meeting on March 31, the European Commission urged member nations to encourage citizens to work from home, drive and fly less, and for EU countries to urgently roll out renewables, as it warned of a prolonged energy crisis as a result of the conflict in the Gulf (Politico). EU energy chief Dan Jørgensen warned Europe was facing a “very serious situation” with no clear end in sight. According to Newsweek, ”the urgency of the talks reflects growing fears that the current energy situation could surpass even the oil crisis of the 1970s. Some officials and analysts warn that the economic fallout could even rival the disruption caused by the COVID‑19 pandemic.”

With inflation expected to rise sharply in the coming months, the European Central Bank is suddenly more likely to tighten interest rates than ease further, thereby increasing the odds of recession. As a net energy exporter, the U.S. is more likely to experience slower growth than a recession, absent a sustained oil shock or sharper labor market deterioration.

Downside scenarios are tied to prolonged oil prices holding above $100 per barrel for much of the year. Most base case forecasts assume that energy prices will stabilize in the coming months, which implies that overall inflation will continue trending lower, …but at a slower pace than previously forecasted. Again, this outlook feels overly optimistic with the Strait of Hormuz effectively closed as the conflict enters its second month.

Despite the uncertainty, the Fed’s March “dot plot” continues to signal one rate cut in 2026 and another in 2027. At the same time, dispersion of the dots within the projection has increased, reflecting a widening range of opinion among committee members.

The March Bloomberg survey indicated U.S. economists believe GDP growth had rebounded slightly in the first quarter but will generally hover around +2.0% in subsequent periods through the end of 2027. The median inflation forecast shows core PCE peaking at +3.0% in Q2, before gradually falling to +2.3% by the second quarter of next year, while unemployment is expected to hold steady within one-tenth of the current 4.4% rate. These same economists expect the Fed will respond with 25 basis point cuts in each of the last two quarters of 2026, a slightly more aggressive timeframe than Fed officials signaled at the March FOMC meeting.

The nation’s economists and Fed officials expect two rate cuts (timing uncertain), but the bond market hasn’t priced-in a single move. For both policymakers and investors, the overriding question for the remainder of the year is whether external shocks fade away or persist. Until there’s more clarity, caution remains the appropriate stance. With this in mind, the bond market is right.

About Scott McIntyre, CFA

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Scott McIntyre specializes in investment management services and is responsible for the management, oversight and trade supervision of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Scott also provides investment advice and consulting, reviews local government investment policies, formulates overall investment strategies, evaluates account performance and oversees the day-to-day operations. He is a member of the Chartered Financial Analyst (CFA) Institute and a CFA Charterholder, a two-term advisor to the GFOA Treasury and Investment Management (TIM) committee, a Registered Investment Advisor, and holds FINRA Series 7, 24, 63, and 65 licenses.

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Scott McIntyre specializes in investment management services and is responsible for the management, oversight and trade supervision of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Scott also provides investment advice and consulting, reviews local government investment policies, formulates overall investment strategies, evaluates account performance and oversees the day-to-day operations. He is a member of the Chartered Financial Analyst (CFA) Institute and a CFA Charterholder, a two-term advisor to the GFOA Treasury and Investment Management (TIM) committee, a Registered Investment Advisor, and holds FINRA Series 7, 24, 63, and 65 licenses.

About Greg Warner, CTP

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Greg Warner specializes in investment management services and is responsible for the management and oversight of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Greg coordinates all client services and portfolio management duties, including security evaluation and portfolio analysis, trading, investment reporting, board presentations, and monitoring of broker-dealer relationships. He is an advisory committee member to the Texas Association of Counties, a member of the Government Treasurers’ Organization of Texas (GTOT), a Registered Investment Advisor, a Certified Treasury Professional (CTP) and holds FINRA Series 7, 63, and 65 licenses.

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Greg Warner specializes in investment management services and is responsible for the management and oversight of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Greg coordinates all client services and portfolio management duties, including security evaluation and portfolio analysis, trading, investment reporting, board presentations, and monitoring of broker-dealer relationships. He is an advisory committee member to the Texas Association of Counties, a member of the Government Treasurers’ Organization of Texas (GTOT), a Registered Investment Advisor, a Certified Treasury Professional (CTP) and holds FINRA Series 7, 63, and 65 licenses.

About Matt Harris, CFA

As HilltopSecurities Asset Management’s Senior Portfolio Advisor, Matt Harris specializes in investment management services for public sector municipal clients. He developed his experience in the banking industry, supporting balance sheet management, interest rate risk analysis, liquidity planning, and investment strategy implementation. At HilltopSecurities, he works closely with clients to develop and implement customized investment strategies, oversees account documentation and reporting, and assists clients with the public funds depository review process, including competitive RFP evaluations. Harris is a member of the CFA Institute and a CFA Charterholder, a Registered Investment Advisor, and holds FINRA Series 7, 63, and 66 licenses.

As HilltopSecurities Asset Management’s Senior Portfolio Advisor, Matt Harris specializes in investment management services for public sector municipal clients. He developed his experience in the banking industry, supporting balance sheet management, interest rate risk analysis, liquidity planning, and investment strategy implementation. At HilltopSecurities, he works closely with clients to develop and implement customized investment strategies, oversees account documentation and reporting, and assists clients with the public funds depository review process, including competitive RFP evaluations. Harris is a member of the CFA Institute and a CFA Charterholder, a Registered Investment Advisor, and holds FINRA Series 7, 63, and 66 licenses.

The paper/commentary was prepared by HilltopSecurities (HTS). It is intended for informational purposes only and does not constitute legal or investment advice, nor is it an offer or a solicitation of an offer to buy or sell any investment or other specific product. Information provided in this paper was obtained from sources that are believed to be reliable; however, it is not guaranteed to be correct, complete, or current, and is not intended to imply or establish standards of care applicable to any attorney or advisor in any particular circumstances. The statements within constitute the views of HTS as of the date of the document and may differ from the views of other divisions/departments of Hilltop Securities Inc. and its affiliates. In addition, the views are subject to change without notice. This paper represents historical information only and is not an indication of future performance. This material has not been prepared in accordance with the guidelines or requirements to promote investment research, it is not a research report and is not intended as such. Sources available upon request.

Hilltop Securities Inc. is a registered broker-dealer, registered investment adviser and municipal advisor firm that does not provide tax or legal advice. HTS is a wholly owned subsidiary of Hilltop Holdings, Inc. (NYSE: HTH) located at 717 N. Harwood St., Suite 3400, Dallas, Texas 75201, (214) 859-1800, 833-4HILLTOP.