click below to login to your secure account

By Tom Kozlik

Head of Public Policy and Municipal Strategy

Hilltop Securities Inc.

Some see only the obstacles in the current market environment. For fixed income and municipal investors, an important element to recognize is that yields remain attractive and they are still higher than we expected they would be in 2026. Most expected yields to drift lower in 2026, but the escalation in the Middle East, and the stop-and-start nature of the negotiations, has kept uncertainty in the market and kept rates from sliding steadily lower.

Economic analysis has become more measured, and in some corners even slightly more negative. For example, at the end of March, Mark Zandi the chief economist at Moody’s Analytics said, “Recession is a real threat here.” He put the odds of a recession over the next 12 months at 49%. Meanwhile, on Sunday afternoon Zandi wrote, “My angst around the possibility of a recession continues to rise.”

The obstacles are real, and they can hit growth, inflation, and policy at the same time. But they also help explain why municipals are still offering an entry point that looked unlikely a few months ago.

Believe it or not, there is a U.S. Federal Open Market Committee (FOMC) meeting coming up at the end of the month. The next scheduled FOMC announcement will be April 29. In March, the Fed remained on “hold” as it cited increased uncertainty tied to the escalation of conflict in the Middle East. They left the target federal funds rate unchanged, as expected, in a range of 3.50%-3.75%.

Most expect the Fed to hold steady again on April 29. Many are also anticipating no action on June 17 or on July 29. The first potential cut could come as early as Sept. 16, but that is far enough away to be highly conditional on geopolitics and data. Market participants and observers are trying to estimate the total impact that energy and energy prices could have in the coming weeks and months. We expect a wider array of potential outcomes for rates than we had earlier in the year as a result.

Some economic data, including the inflation data reported Friday, has moved higher. Better than expected job market numbers for March gave the Fed some breathing room, and kept the near-term focus on the Middle East and how the news from there is likely to impact energy, inflation, costs and consumer sentiment. Two potential big-picture paths are in play. The first is that the shock fades, and rates can drift lower over time. The second is that the shock lingers long enough to consistently impact behavior, pricing, and policy expectations. The difference between those two paths is the difference between a late-year cut that feels normal, like many expected at the beginning of the year, and a late-year cut that never arrives.

Lawmakers are returning to Washington D.C. The Senate returned yesterday and the House returned to session today. Attention is starting to narrow on legislative goals. Negotiations with Iran are dominating the news cycle and crowding out almost everything else. That is a problem considering mid-term elections are in November. The Republican Party largely wants to remind voters about the Big Beautiful Bill of 2025’s tax benefits, especially now that it is tax season.

It is possible lawmakers could restart debate about the SAVE America Act, even though most Republicans do not think it is likely to pass. It remains important to President Trump. Republicans also remain divided on how to end the Department of Homeland Security shutdown, and at issue could be future paychecks for TSA officers. There could be new life for the prospects of a reconciliation spending deal in 2026. The House could be positioning for a signal from the Senate, and the Senate Majority Leader already said it is possible. We are watching for the possibility for a reconciliation agreement especially because of the potential threat to the municipal bond tax-exemption it could pose.

For municipal bond investors the obstacles are still creating one of the better opportunities to capture additional yield than we expected at the start of this year. Early in 2026 we saw investors, understandably, choosing stability by funneling investment dollars into tax-exempt and taxable municipal bonds even as some investors pared back equity market exposure.

We have been reminding investors that credit selection still matters. We wrote and still see signs that 2026 is shaping up as a corrective period for municipal bond credit quality, where credit selection matters more, and sector differentiation is widening.

The team of HilltopSecurities credit analysts took a close sector-by-sector look during our 2026 Municipal Market Sector Credit Outlooks, where we highlighted that 2026 is a “discipline year” for municipals. The post 2020 and 2021 subsidy glow is fading. Rating momentum is normalizing, and outcomes will increasingly be driven by issuer‑by‑issuer fundamentals.

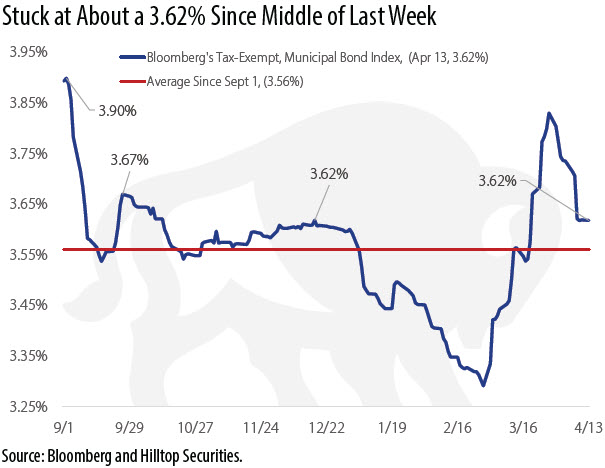

The more important opportunity, amidst all the obstacles like monetary policy, the macro-economic environment, fiscal policy, geopolitics and municipal credit is the level of absolute yields we are seeing in mid-April. We got a second look at last year’s yields a few weeks ago. This market is still offering investors an excellent entry point. The Bloomberg Municipal Bond Index’s yield has been hovering around a 3.62% since the middle of last week. It was as high as a 3.83% at the end of March. The 10-year Municipal Market Data (MMD) AAA benchmark yield ended Monday at a 2.95% yield.

The supply and demand dynamic is rather balanced. March issuance was very heavy at about $50 billion, and issuance from last week at $10 billion is low compared to this week’s roughly $14 billion of primary market offerings. Primary supply is still plentiful. On the demand side, we have seen mostly very strong interest in municipals continue in 2026. A net $18 billion has flowed into municipal funds this year, per Lipper data. Last week was $866 million and the week before $923 billion. Often flows turn negative during or prior to tax time, and although the amounts have lessened slightly, we are still seeing considerable interest in municipals via institutional fund flows.

Readers may view all of the HilltopSecurities Municipal Commentary here.

![]() As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or tom.kozlik@hilltopsecurities.com.

As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or tom.kozlik@hilltopsecurities.com.

The paper/commentary was prepared by HilltopSecurities (HTS). It is intended for informational purposes only and does not constitute legal or investment advice, nor is it an offer or a solicitation of an offer to buy or sell any investment or other specific product. Information provided in this paper was obtained from sources that are believed to be reliable; however, it is not guaranteed to be correct, complete, or current, and is not intended to imply or establish standards of care applicable to any attorney or advisor in any particular circumstances. The statements within constitute the views of HTS Public Finance as of the date of the document and may differ from the views of other divisions/departments of Hilltop Securities Inc. In addition, the views are subject to change without notice. This paper represents historical information only and is not an indication of future performance. This material has not been prepared in accordance with the guidelines or requirements to promote investment research, it is not a research report and is not intended as such. Sources available upon request.

Hilltop Securities Inc. is a registered broker-dealer, registered investment adviser and municipal advisor firm that does not provide tax or legal advice. HTS is a wholly owned subsidiary of Hilltop Holdings, Inc. (NYSE: HTH) located at 717 N. Harwood St., Suite 3400, Dallas, Texas 75201, (214) 859-1800, 833-4HILLTOP.