click below to login to your secure account

By Tom Kozlik

Head of Public Policy and Municipal Strategy

Hilltop Securities Inc.

2026 opened with optimism, but by late February investors were operating with rising uncertainty and thin conviction, even as major equity indices marked highs and day‑to‑day swings intensified. March added fuel as the conflict involving the United States, Israel, and Iran escalated and oil prices jumped, a reminder that geopolitics can still move markets quickly.

The unease has extended in April so far. Rates have remained elevated, risk appetite is unsettled, and neither policy nor incoming data has offered a convincing release valve. An even more impactful pressure point sits elsewhere. Investors are beginning to recognize artificial intelligence (AI) not only as an investing theme, but potentially as a general‑purpose technology.

Geopolitics can change the next inflation print and the next turn in rates. AI has the potential to reshape the economics of production, management, and labor, and it could reshape infrastructure needs and investment priorities across sectors. That is the distinction markets are now being forced to consider, even with the headlines pulling attention in the other direction.

Artificial intelligence is no longer being treated merely as an intriguing productivity aid or just the next wave of experimentation and tech-hype. More investors, and market observers are beginning to see it as a significant general-purpose technology, a label reserved for technologies that spread across industries, improve over time, lower costs, and eventually change how firms operate and how economies grow. The printing press did not merely make books cheaper. The steam engine and railroads did not only move goods more quickly. Electricity did not just improve lighting. The personal computer and internet did not simply make communication faster. Each altered the structure of economic life around itself.

That is why the market’s current anxiety around AI should be taken seriously but weighed carefully. Investors are not simply reacting to a new version of a chatbot, or the latest round of hyper-scaler or Silicon Valley theater. They are confronting the possibility that AI becomes a foundational layer of economic life, with consequences that run through labor, infrastructure, energy demand, capital spending, corporate organization, and the long-term potential architecture of economic growth.

To understand this moment, it helps to separate the market reaction from the deeper process unfolding beneath it. An overlap period has already begun and will continue whether markets, observers or individuals fully appreciate it or not. It is the stage in which the old system still operates even as a new layer is built into it. A recent transition offers a useful comparison.

In the late 1990s, the internet arrived with unique sounds. A dial tone. Then clicks. Then that staccato chatter and steady hiss as machines tried to agree on how to talk. You could hear the connection being made, and you could feel how fragile it was. If somebody picked up the kitchen phone, the whole thing fell apart.

By the 2010s, the internet had stopped making noise. Not because it disappeared, but because it did the opposite. It became the quiet layer everything else sat on.

That layer has a name: substrate.

A substrate is the base layer beneath everything else. The part you stop talking about because you assume it is there. Roads became substrate. Plumbing became substrate. Electricity became substrate. You tend to notice those systems when they fail, when they are constrained, or when someone is rebuilding them beneath your feet.

That reflection matters because we may be watching the early stages of a similar shift now. But this time the new layer is not connectivity. It is cognition.

Artificial intelligence is moving from an intriguing tool you can choose to use toward something closer to a support layer for day-to-day work. Over time it could or will become embedded, assumed, and quiet. Then, almost all at once, it will become difficult to imagine operating without. This integration won’t occur overnight. But it may occur faster than the internet and personal computer (PC) integrated into everyday life, because this AI layer rides on top of digital systems that are already everywhere.

That does not mean the old forces shaping the municipal bond market, public finance and the economy suddenly disappear. Geopolitics still matters. The Federal Reserve still matters. Federal fiscal policy still matters. Credit quality, issuance, housing, employment, and the long after-effects of the Post-Golden Realignment still matter. The old levers still move the machine, for now. But AI is beginning to sit alongside them, not as a novelty, but as a force that may reshape how the machine is constructed, operates and where new opportunities and strains could emerge.

Now, in April 2026, a growing share of investors are beginning to recognize this AI Overlap Period and to understand that the technology is being woven into the substrate in much the same way the personal computer, the internet, and later social media embedded themselves into existing systems. That overlap, and the strain it introduces as old assumptions collide with new capabilities, contributed to market anxiety early in the year. It also remains a source of uncertainty as investors look ahead, unsure how quickly, unevenly, and consequentially this transition will unfold.

The market anxiety that developed in January and February did not appear out of thin air. It had specific triggers. New automation tools from Anthropic, the company behind the Claude suite of products, sharpened concerns across multiple asset classes, especially in software and adjacent industries, as investors reassessed how quickly AI could pressure employment, margins, and business models. Then a widely shared “scenario exercise” from Citrini Research, The 2028 Global Intelligence Crisis: A Thought Exercise in Financial History, from the Future, spread rapidly by imagining a world in which AI capabilities keep improving while wages and consumer spending weaken. The piece featured a hypothetical 10.2% unemployment rate and a 38% drawdown in the S&P 500 from late-2026 highs. Citrini’s “scenario exercise” was purposefully provocative. It was also fictional, and somewhat far-fetched.

That distinction matters greatly. The Citrini piece is best understood as a “scenario exercise,” not actionable research and certainly not as a base case. The situation contemplated was two years in the future and depends on a long chain of assumptions breaking in the same direction on a very fast timeline. It also very much underweights the real-world frictions already slowing the translation from technical progress to economy-wide disruption, including quick, but uneven adoption, constrained compute and power capacity, and the time it takes to retool.

The pushback that followed the release of the Citrini exercise helped clarify the real argument now taking place in markets. Citadel Securities argued that rapid technological progress does not automatically translate into rapid economic adoption, especially when scaling depends on physical capacity such as semiconductors, data centers, and energy infrastructure. Paul Krugman, the Nobel Prize–winning economist and longtime former New York Times columnist, made a parallel point from a different angle. Dramatic narratives can move markets and audiences even when they offer little that is verifiable. Krugman pointed to Orson Welles’ 1938 War of the Worlds broadcast as a reminder.

That is where discipline and understanding matter. Markets move on what feels plausible long before they settle on what is true. Right now, the central backdrop for public finance and the rest of the economy, is not simply AI optimism or AI fear. It is the overlap period between a still-functioning old system and a fast-improving new one. That is enough to force investors to rethink what is durable, what is fragile, and what could change.

AI feels revolutionary, but much of the measurable evidence still looks familiar in the beginning of 2026. That is the first thing investors need to keep straight. The data does not yet show or forecast an AI-driven labor-market asteroid strike.

That gap between perception and evidence is not a contradiction. It is a marker of where we are in the tech transition. Capability is growing quickly. Yet adoption, while also occurring quickly compared to past technologies, is probably lagging outside of the technology world as leaders, workers, and the economy still consider and absorb the potential for change.

So far, the labor-market data does not show an economy already torn apart by AI, but there has been an impact. The labor-market effects are real, but we are still in the very early innings. The loudest claims, like in mid-March when the CEO of ServiceNow said AI agents could send college grad unemployment over 30%, make it sound like the jobs apocalypse already arrived. The actual data says something more nuanced.

Stanford’s “Canaries in the Coal Mine” finds meaningful employment declines for early-career workers in AI-exposed occupations such as software development and customer support, and that the labor market impact so far is concentrated, not universal. The canaries are signaling, but the whole mine has not collapsed. The nuance matters here and it will continue to matter. The Stanford analysis results suggest AI is already reshaping entry-level hiring in some corners of the economy, especially where it automates tasks rather than augments them.

Economists who once dismissed AI’s labor market implications are now paying closer attention, without abandoning the view that this transition can be broadly beneficial. Most still see little evidence of widespread disruption, but they are increasingly open to the idea that change may arrive incrementally rather than all at once. As the New York Times observed last week, the question is less whether AI will reshape work than how and when those effects become visible. That framing leaves room for productivity gains, new roles, and adaptation, even as early signals at the margins begin to register.

McKinsey offers a pragmatic transition narrative in Agents, Robots, and Us: Skill Partnerships in the Age of AI, arguing that, “AI-powered automation will change work, but people will remain indispensable” and that “Human skills will evolve, not disappear, as people work closely with AI.” In other words, the transition is less about replacement than reorganization, with AI reshaping how work is done rather than removing people from it. Taken together, the picture is not one of mass displacement, but of a slow sorting of tasks, skills, and responsibilities as humans and machines work alongside each other.

A similar assessment appears in a new report, “AI Will Reshape More Jobs Than It Replaces,” from Boston Consulting Group, published last week, which argues that AI is more likely to reshape jobs than eliminate them outright. Their analysis points to roles changing faster than headcounts, with tasks shifting, expectations rising, and skill requirements evolving unevenly across sectors. The overall message is measured, not dramatic.

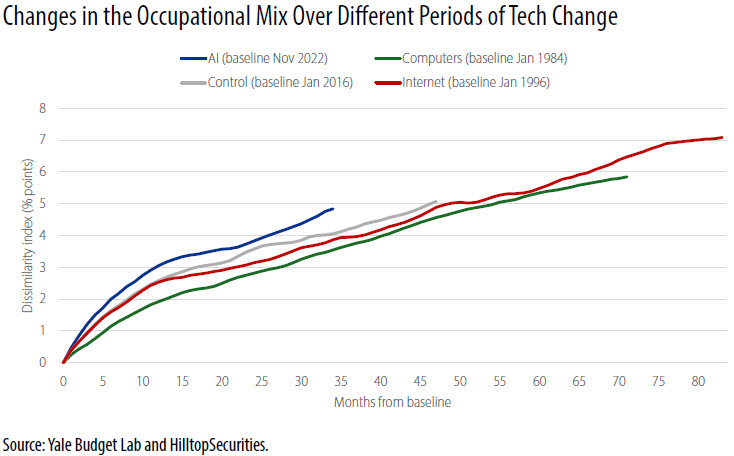

We can also see that the comparison of occupational change, via The Yale Budget Lab is a useful reality check. The shift in the occupational mix has been meaningful, but it still sits within a range that looks broadly comparable to earlier technological transitions. The usage or adoption data we are seeing goes in a similar direction as well.

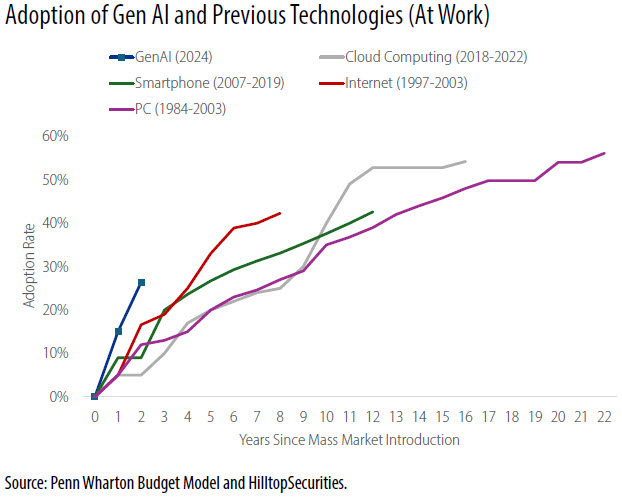

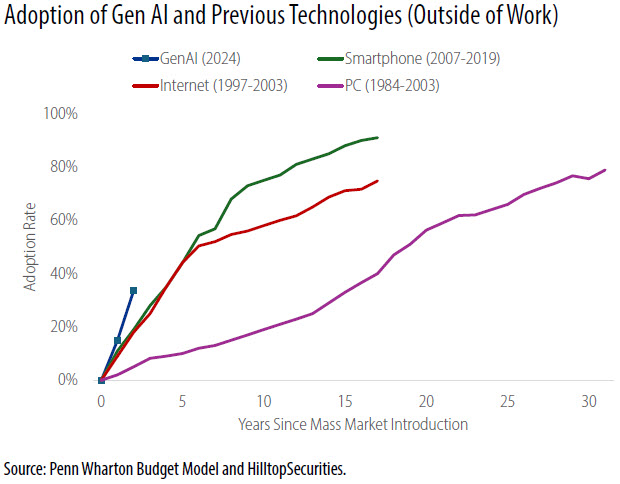

GenAI adoption at work has been fast and real, but the early curve still looks more like the spread of other important technologies rather than a clean break from history, according to The Projected Impact of Generative AI on Future Productivity Growth by the Penn Wharton Budget Model. The usage data says AI adoption is rising, experimentation is broadening, and workflow integration is underway. The market is increasingly assuming that AI may eventually go deeper than prior tools into white-collar work, reach closer to cognition itself, and force firms to redesign not only tasks but headcount, management, and business architecture. Both ideas can be true at the same time. A general-purpose technology can be transformative over time without immediately producing a dramatic macroeconomic signature.

We should expect AI to rearrange tasks first, and then, over time, reshape some jobs. That is why the earlier line in this report is worth reiterating again: AI has the potential to reshape the economics of production, management, and labor, and to reshape infrastructure needs and investment priorities across sectors.

The World Economic Forum’s (WEF) Future of Jobs Report 2025 puts hard numbers around the potential transition, estimating that disruption will touch about 22% of today’s jobs by 2030, with roughly 170 million roles created and 92 million displaced, for a net gain of 78 million, globally. The WEF report also makes the core constraint explicit. Nearly 40% of job skills are expected to change, 63% of employers cite skills gaps as their top barrier, and 59 out of 100 workers are projected to need reskilling or upskilling by 2030.

Taken together, the data and expert expectations point to a transition that is underway but still incomplete. The market is not reacting only to what the data shows today. It is reacting to what AI might become over time. The hard part is keeping the present separate from the possible while the evidence is still early and the trajectory depends on diffusion and constraints. The range of outcomes is wide, but the more likely path is one in which human skills evolve and improve as AI reshapes workflows and task design more than it replaces people.

Early macro data can look ordinary even when a meaningful shift is underway. Massive technological change often shows up first with early adopters, then moves into workflows, then starts changing incentives and, eventually, the structure of firms, governments and institutions evolves. That path is usually uneven, and the aggregate numbers typically catch up only after the rewiring is already in motion. And this does take time.

Even with oil and the Middle East dominating the headlines, the deeper issue confronting markets is structural. Investors are managing near-term geopolitical risk, but they are also beginning to grapple with AI as the early emergence of a general-purpose technology, one that can pull new industries into existence and reshape labor, capital spending, infrastructure, corporate organization, and the long-run architecture of growth. That is why unease feels so persistent right now. Near-term shocks are arriving on top of a slower, more consequential transition that markets are only starting to confront. This is the AI Overlap Period.

Readers may view all of the HilltopSecurities Municipal Commentary here.

![]() As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or tom.kozlik@hilltopsecurities.com.

As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or tom.kozlik@hilltopsecurities.com.

The paper/commentary was prepared by HilltopSecurities (HTS). It is intended for informational purposes only and does not constitute legal or investment advice, nor is it an offer or a solicitation of an offer to buy or sell any investment or other specific product. Information provided in this paper was obtained from sources that are believed to be reliable; however, it is not guaranteed to be correct, complete, or current, and is not intended to imply or establish standards of care applicable to any attorney or advisor in any particular circumstances. The statements within constitute the views of HTS Public Finance as of the date of the document and may differ from the views of other divisions/departments of Hilltop Securities Inc. In addition, the views are subject to change without notice. This paper represents historical information only and is not an indication of future performance. This material has not been prepared in accordance with the guidelines or requirements to promote investment research, it is not a research report and is not intended as such. Sources available upon request.

Hilltop Securities Inc. is a registered broker-dealer, registered investment adviser and municipal advisor firm that does not provide tax or legal advice. HTS is a wholly owned subsidiary of Hilltop Holdings, Inc. (NYSE: HTH) located at 717 N. Harwood St., Suite 3400, Dallas, Texas 75201, (214) 859-1800, 833-4HILLTOP.