click below to login to your secure account

By Matt Harris, CFA

Senior Portfolio Advisor

HilltopSecurities Asset Management

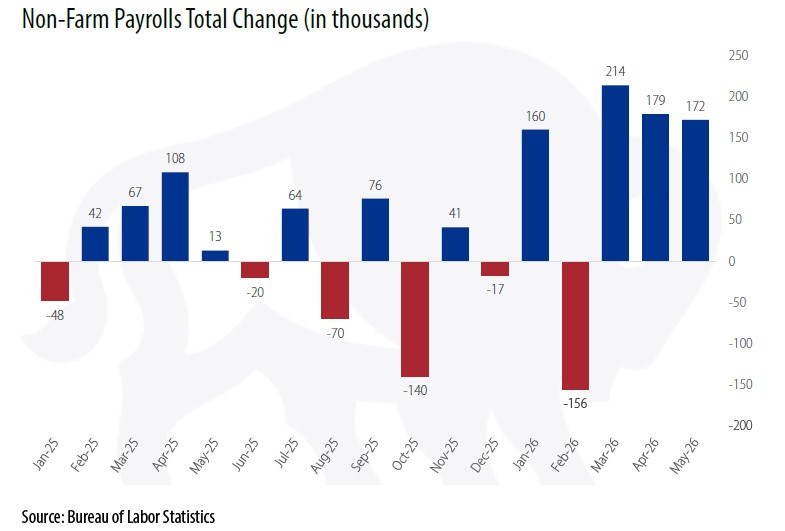

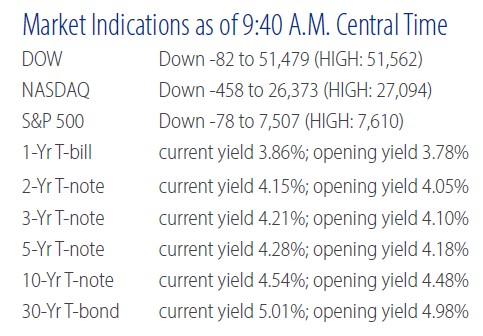

The Bureau of Labor Statistics reported a much stronger than expected May jobs report today, pushing bond yields higher across the curve. Nonfarm payrolls rose by 172k, well above the consensus forecast of 88k and one of the largest upside surprises in recent years. Revisions added another 93k jobs to the prior two months, lifting the three-month average to 188k, a sharp rebound from just 6k in February.

Leisure and hospitality led job creation with a 70k increase, marking its strongest gain in over three years. Healthcare and social assistance, a consistent driver of employment growth, also contributed meaningfully with 37k new jobs. Manufacturing added jobs as well, alongside gains in construction, pointing to continued strength in goods-producing sectors tied to areas such as data centers, defense spending, and inventory rebuilding. Government hiring was a positive contributor for the month, with state and local employment rising by 52k. However, some sectors showed signs of weakness. Financials, information technology, trade, and transportation all posted declines.

Wage growth showed further signs of cooling. Average hourly earnings rose 0.3% in May, in line with expectations, while year-over-year growth slowed to 3.4% from 3.6% in April, matching the slowest pace since 2021. Economists have been closely watching whether tight labor market conditions would continue to drive wage gains, particularly as inflation has at times outpaced pay growth. For now, the moderation in wages suggests that while the labor market remains firm, compensation pressures are not accelerating in a way that would reinforce broader inflation, reducing the risk of a self-sustaining wage-price spiral.

From the household survey, employment increased by 149k while the labor force grew by 83k, both marking solid gains on the month. The unemployment rate edged slightly lower but held at 4.3% on a rounded basis. The labor force participation rate was unchanged at 61.8%, stabilizing after recent declines, while the employment-to-population ratio also held steady at 59.2%.

Prime-age participation, which focuses on workers aged 25 to 54, edged higher, suggesting strength in the core labor force. The underemployment rate, a broader measure of unemployment that includes those working part-time for economic reasons and discouraged workers ticked lower, also pointing to improvement in labor market slack.

Earlier this week, other labor market data pointed in a similar direction. The ADP report showed a 122k increase in private sector jobs, with gains across firms of all sizes. Meanwhile, the Job Openings and Labor Turnover Survey (JOLTS) showed job openings rising by 731k in April to 6.62 million, the highest level since 2024.

The recent spate of positive jobs data shows a labor market regaining momentum across sectors after last year’s period of near-zero job growth. Strong headline gains, coupled with upward revisions shift the focus back toward inflation rather than employment weakness. Markets reflected that shift, with Treasury yields moving higher and rate expectations firming as investors priced in a greater likelihood of Fed tightening by year-end. While some underlying indicators still point to caution, including softer sentiment and uneven hiring, the near-term takeaway is labor market strength is not the concern, and the Fed’s attention remains firmly focused on inflation.

About Scott McIntyre, CFA

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Scott McIntyre specializes in investment management services and is responsible for the management, oversight and trade supervision of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Scott also provides investment advice and consulting, reviews local government investment policies, formulates overall investment strategies, evaluates account performance and oversees the day-to-day operations. He is a member of the Chartered Financial Analyst (CFA) Institute and a CFA Charterholder, a two-term advisor to the GFOA Treasury and Investment Management (TIM) committee, a Registered Investment Advisor, and holds FINRA Series 7, 24, 63, and 65 licenses.

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Scott McIntyre specializes in investment management services and is responsible for the management, oversight and trade supervision of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Scott also provides investment advice and consulting, reviews local government investment policies, formulates overall investment strategies, evaluates account performance and oversees the day-to-day operations. He is a member of the Chartered Financial Analyst (CFA) Institute and a CFA Charterholder, a two-term advisor to the GFOA Treasury and Investment Management (TIM) committee, a Registered Investment Advisor, and holds FINRA Series 7, 24, 63, and 65 licenses.

About Greg Warner, CTP

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Greg Warner specializes in investment management services and is responsible for the management and oversight of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Greg coordinates all client services and portfolio management duties, including security evaluation and portfolio analysis, trading, investment reporting, board presentations, and monitoring of broker-dealer relationships. He is an advisory committee member to the Texas Association of Counties, a member of the Government Treasurers’ Organization of Texas (GTOT), a Registered Investment Advisor, a Certified Treasury Professional (CTP) and holds FINRA Series 7, 63, and 65 licenses.

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Greg Warner specializes in investment management services and is responsible for the management and oversight of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Greg coordinates all client services and portfolio management duties, including security evaluation and portfolio analysis, trading, investment reporting, board presentations, and monitoring of broker-dealer relationships. He is an advisory committee member to the Texas Association of Counties, a member of the Government Treasurers’ Organization of Texas (GTOT), a Registered Investment Advisor, a Certified Treasury Professional (CTP) and holds FINRA Series 7, 63, and 65 licenses.

About Matt Harris, CFA

As HilltopSecurities Asset Management’s Senior Portfolio Advisor, Matt Harris specializes in investment management services for public sector municipal clients. He developed his experience in the banking industry, supporting balance sheet management, interest rate risk analysis, liquidity planning, and investment strategy implementation. At HilltopSecurities, he works closely with clients to develop and implement customized investment strategies, oversees account documentation and reporting, and assists clients with the public funds depository review process, including competitive RFP evaluations. Harris is a member of the CFA Institute and a CFA Charterholder, a Registered Investment Advisor, and holds FINRA Series 7, 63, and 66 licenses.

As HilltopSecurities Asset Management’s Senior Portfolio Advisor, Matt Harris specializes in investment management services for public sector municipal clients. He developed his experience in the banking industry, supporting balance sheet management, interest rate risk analysis, liquidity planning, and investment strategy implementation. At HilltopSecurities, he works closely with clients to develop and implement customized investment strategies, oversees account documentation and reporting, and assists clients with the public funds depository review process, including competitive RFP evaluations. Harris is a member of the CFA Institute and a CFA Charterholder, a Registered Investment Advisor, and holds FINRA Series 7, 63, and 66 licenses.

The paper/commentary was prepared by HilltopSecurities (HTS). It is intended for informational purposes only and does not constitute legal or investment advice, nor is it an offer or a solicitation of an offer to buy or sell any investment or other specific product. Information provided in this paper was obtained from sources that are believed to be reliable; however, it is not guaranteed to be correct, complete, or current, and is not intended to imply or establish standards of care applicable to any attorney or advisor in any particular circumstances. The statements within constitute the views of HTS as of the date of the document and may differ from the views of other divisions/departments of Hilltop Securities Inc. and its affiliates. In addition, the views are subject to change without notice. This paper represents historical information only and is not an indication of future performance. This material has not been prepared in accordance with the guidelines or requirements to promote investment research, it is not a research report and is not intended as such. Sources available upon request.

Hilltop Securities Inc. is a registered broker-dealer, registered investment adviser and municipal advisor firm that does not provide tax or legal advice. HTS is a wholly owned subsidiary of Hilltop Holdings, Inc. (NYSE: HTH) located at 717 N. Harwood St., Suite 3400, Dallas, Texas 75201, (214) 859-1800, 833-4HILLTOP.