click below to login to your secure account

By Matt Harris, CFA

Senior Portfolio Advisor

HilltopSecurities Asset Management

A wave of economic data this morning showed economic growth revised higher while business investment remained firm. Meanwhile, strong spending alongside elevated inflation continues to cloud the Fed’s outlook, as markets appear to be leaning toward lower inflation readings ahead.

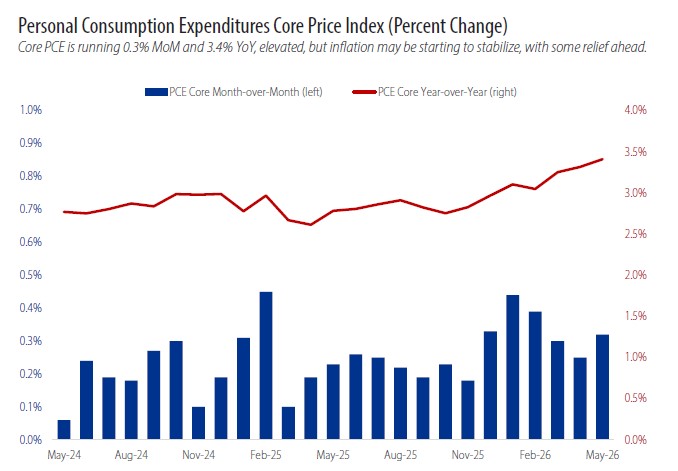

May PCE Inflation

The Fed’s preferred inflation measure rose 0.4% in May, below the 0.5% expectation, while core PCE increased 0.3%, in line with forecasts. However, the Bureau of Economic Analysis also revised the April PCE core higher, reinforcing recent price pressure.

On a year-over-year basis, headline PCE rose to 4.1%, the highest in over three years, while core increased to 3.4%. The monthly readings were soft enough to ease near-term concerns, but the broader trend still reflects sticky inflation.

The early read on June inflation is more encouraging. The Cleveland Fed’s Inflation Nowcast estimates June CPI at 0.0% month-over-month and core CPI at 0.2%, while PCE is tracking near 0.1% and core PCE around 0.3%. On a year-over-year basis, the nowcast shows headline PCE easing to 3.8% in June, while core PCE is estimated at 3.3%, slightly below May’s reading. If these estimates hold, May could be the near-term peak in inflation, giving markets some confidence that the worst of the recent price pressures might be behind us.

Personal Income and Spending

Both personal income and spending rose 0.7% in May, beating expectations. After adjusting for inflation, real spending increased 0.3%, a modest improvement from April that should support second-quarter growth.

However, spending continues to outpace real income growth, suggesting consumers are maintaining their ability to purchase goods and services but gradually losing purchasing power and drawing down savings.

Q1 GDP Revision

First-quarter GDP was revised higher to 2.1% from 1.6%, though the breakdown was less encouraging. Consumer spending was revised lower, while a significant downward revision to imports accounted for most of the improvement in growth.

Net exports were a much smaller drag in the final estimate. The takeaway is that headline growth was stronger than initially reported, but underlying demand was somewhat softer.

Durable Goods Orders

Durable goods orders, as reported by the Census Bureau, fell 4.5% in May following an 8.5% gain in April, reflecting volatility in aircraft orders. The more important signal came from core capital goods orders (nondefense ex-aircraft), which rose 1.6% and have remained strong in recent months.

This points to continued momentum in business investment, suggesting the capital spending cycle remains a positive contributor to overall economic growth.

Market Reaction

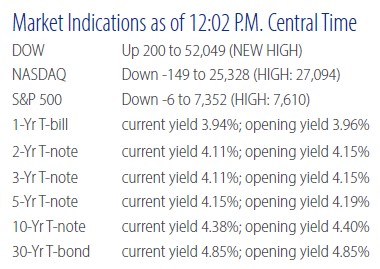

Markets reacted positively to the inflation data, with Treasury yields moving lower on the day, down about 8–10 basis points over the past two sessions in a modest rally. Looking ahead, tomorrow’s University of Michigan Consumer Sentiment report will provide an updated read on confidence and inflation expectations. The June final measure is expected to improve from May’s all-time low, though sentiment remains historically weak. Overall, rate expectations have edged lower, with markets pulling back modestly on the likelihood of additional Fed tightening.

About Scott McIntyre, CFA

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Scott McIntyre specializes in investment management services and is responsible for the management, oversight and trade supervision of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Scott also provides investment advice and consulting, reviews local government investment policies, formulates overall investment strategies, evaluates account performance and oversees the day-to-day operations. He is a member of the Chartered Financial Analyst (CFA) Institute and a CFA Charterholder, a two-term advisor to the GFOA Treasury and Investment Management (TIM) committee, a Registered Investment Advisor, and holds FINRA Series 7, 24, 63, and 65 licenses.

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Scott McIntyre specializes in investment management services and is responsible for the management, oversight and trade supervision of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Scott also provides investment advice and consulting, reviews local government investment policies, formulates overall investment strategies, evaluates account performance and oversees the day-to-day operations. He is a member of the Chartered Financial Analyst (CFA) Institute and a CFA Charterholder, a two-term advisor to the GFOA Treasury and Investment Management (TIM) committee, a Registered Investment Advisor, and holds FINRA Series 7, 24, 63, and 65 licenses.

About Greg Warner, CTP

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Greg Warner specializes in investment management services and is responsible for the management and oversight of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Greg coordinates all client services and portfolio management duties, including security evaluation and portfolio analysis, trading, investment reporting, board presentations, and monitoring of broker-dealer relationships. He is an advisory committee member to the Texas Association of Counties, a member of the Government Treasurers’ Organization of Texas (GTOT), a Registered Investment Advisor, a Certified Treasury Professional (CTP) and holds FINRA Series 7, 63, and 65 licenses.

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Greg Warner specializes in investment management services and is responsible for the management and oversight of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Greg coordinates all client services and portfolio management duties, including security evaluation and portfolio analysis, trading, investment reporting, board presentations, and monitoring of broker-dealer relationships. He is an advisory committee member to the Texas Association of Counties, a member of the Government Treasurers’ Organization of Texas (GTOT), a Registered Investment Advisor, a Certified Treasury Professional (CTP) and holds FINRA Series 7, 63, and 65 licenses.

About Matt Harris, CFA

As HilltopSecurities Asset Management’s Senior Portfolio Advisor, Matt Harris specializes in investment management services for public sector municipal clients. He developed his experience in the banking industry, supporting balance sheet management, interest rate risk analysis, liquidity planning, and investment strategy implementation. At HilltopSecurities, he works closely with clients to develop and implement customized investment strategies, oversees account documentation and reporting, and assists clients with the public funds depository review process, including competitive RFP evaluations. Harris is a member of the CFA Institute and a CFA Charterholder, a Registered Investment Advisor, and holds FINRA Series 7, 63, and 66 licenses.

As HilltopSecurities Asset Management’s Senior Portfolio Advisor, Matt Harris specializes in investment management services for public sector municipal clients. He developed his experience in the banking industry, supporting balance sheet management, interest rate risk analysis, liquidity planning, and investment strategy implementation. At HilltopSecurities, he works closely with clients to develop and implement customized investment strategies, oversees account documentation and reporting, and assists clients with the public funds depository review process, including competitive RFP evaluations. Harris is a member of the CFA Institute and a CFA Charterholder, a Registered Investment Advisor, and holds FINRA Series 7, 63, and 66 licenses.

The paper/commentary was prepared by HilltopSecurities (HTS). It is intended for informational purposes only and does not constitute legal or investment advice, nor is it an offer or a solicitation of an offer to buy or sell any investment or other specific product. Information provided in this paper was obtained from sources that are believed to be reliable; however, it is not guaranteed to be correct, complete, or current, and is not intended to imply or establish standards of care applicable to any attorney or advisor in any particular circumstances. The statements within constitute the views of HTS as of the date of the document and may differ from the views of other divisions/departments of Hilltop Securities Inc. and its affiliates. In addition, the views are subject to change without notice. This paper represents historical information only and is not an indication of future performance. This material has not been prepared in accordance with the guidelines or requirements to promote investment research, it is not a research report and is not intended as such. Sources available upon request.

Hilltop Securities Inc. is a registered broker-dealer, registered investment adviser and municipal advisor firm that does not provide tax or legal advice. HTS is a wholly owned subsidiary of Hilltop Holdings, Inc. (NYSE: HTH) located at 717 N. Harwood St., Suite 3400, Dallas, Texas 75201, (214) 859-1800, 833-4HILLTOP.