click below to login to your secure account

By Scott McIntyre

Co-Head of Investment Management

HilltopSecurities Asset Management

The second quarter economic theme was surprisingly uncomplicated. As the war with Iran continued, rising crude oil prices pushed headline inflation higher which drove bond yields upward. At the same time, labor conditions appeared to improve significantly during the spring months which suggested Fed officials could focus solely on their inflation mandate. A new Fed chair took over the FOMC reins at the June meeting, emphasizing the committee’s top priority would be to lower inflation.

However, the economic narrative had already begun to shift in June as the Trump administration once again announced progress had been made in peace negotiations with Iran. As daylight vessel crossings through the Strait of Hormuz gradually resumed, expectations for a lasting ceasefire drove crude oil prices within a few dollars of the pre-war levels. The abrupt drop in energy costs suggests the rise in headline inflation will reverse itself in the coming months, reducing any urgency to preemptively tighten monetary policy.

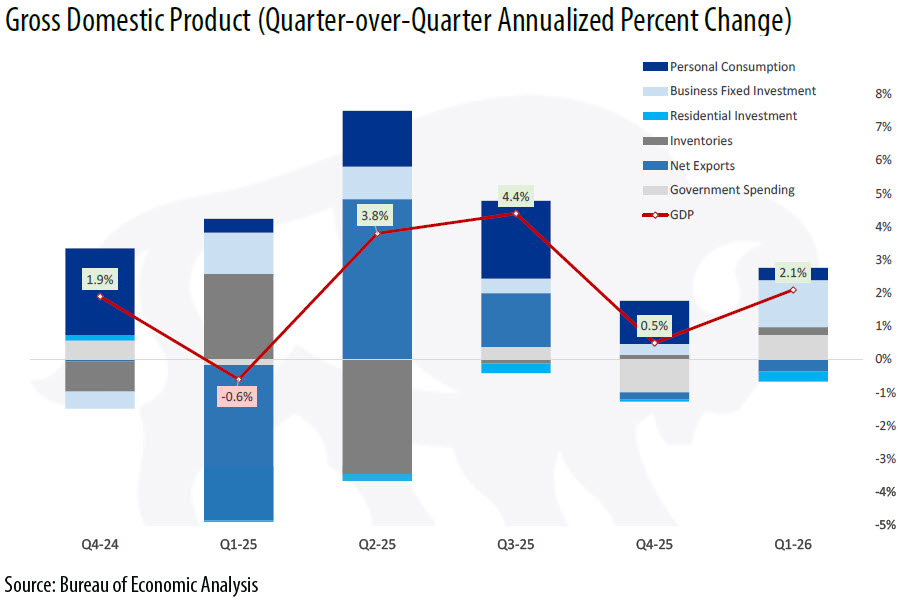

The jury is still out on economic growth. The surging stock market implies a degree of expansion that has yet to be fully reflected in the data. The final measure of first quarter GDP was revised upward from +1.6% to +2.1%, although underlying details weren’t as upbeat. Personal consumption was revised downward from +1.4% to +0.5%, the slowest pace of consumer spending in four years.

The positive counterbalance was Q1 business investment, fueled by the ongoing buildout of artificial intelligence infrastructure. Spending in this category increased at a stunning +10.6% annual rate in the first three months of 2026, up from +2.4% in the previous quarter.

Brisk business investment continued in the second quarter, but consumer capacity appears strained, residential investment is stagnant and a widening trade deficit will be a substantial (though temporary) drag on headline growth. The Atlanta Fed’s GDPNow measure for Q2 was just +1.2% on the first day of July with negative net exports pulling overall growth sharply lower.

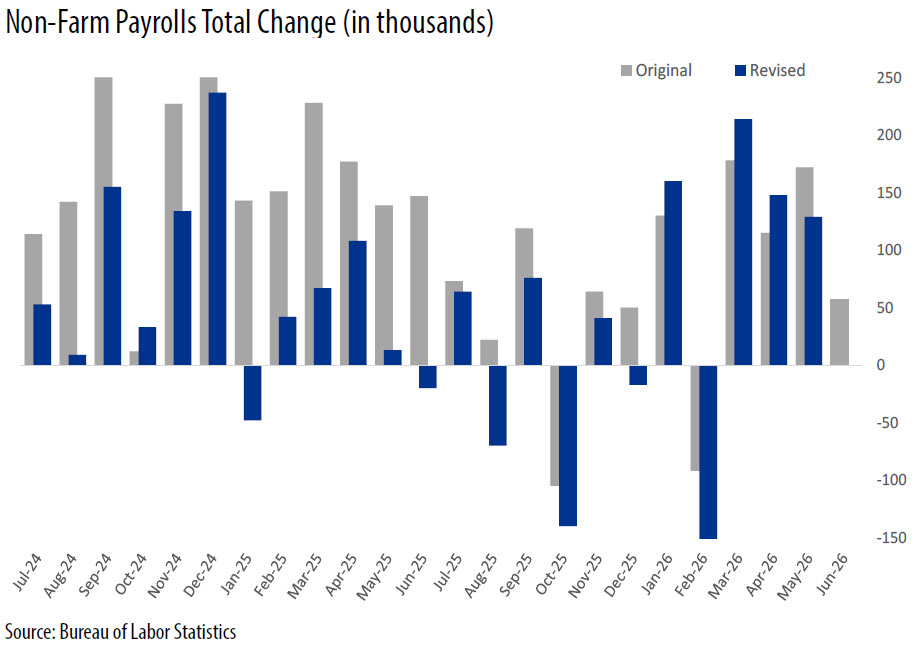

Labor growth had been quite tepid when the year began. The February employment report from the Bureau of Labor Statistics (BLS) showed there had been negative payroll growth (job losses) in five of the past nine months, while nonfarm payrolls since April 2025 had averaged -2k. This apparent weakness in the labor market had kept expectations for rate cuts alive. The narrative swung dramatically in the second quarter as job growth unexpectedly roared back. May payrolls rose +172k, nearly doubling forecasts, while huge upward revisions bolstered the March/April count. The final tally brought the 3-month average to +188k, which effectively dismissed lingering expectations that the Fed would ease in 2026.

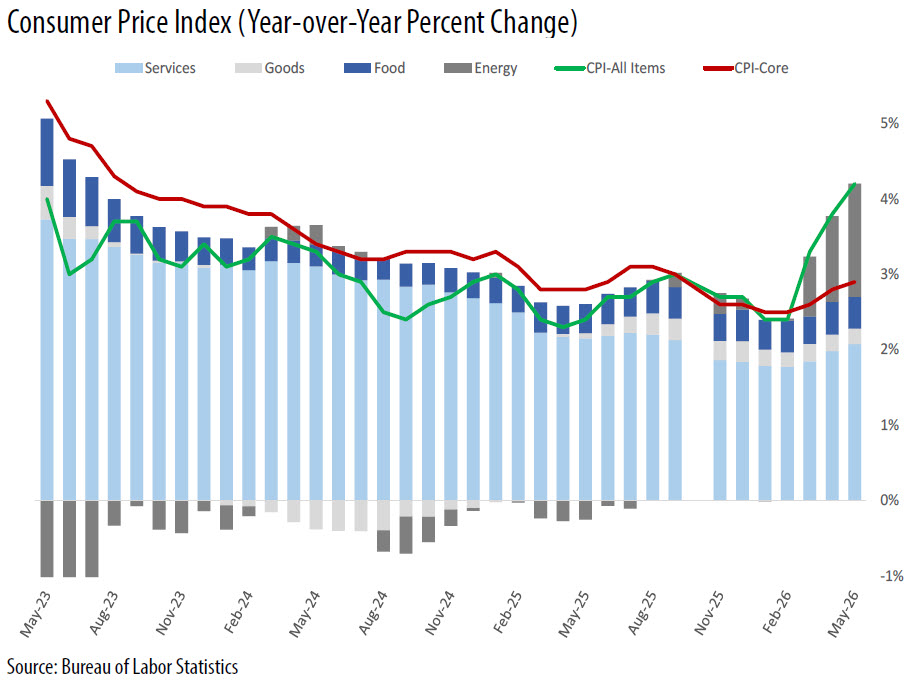

Consumer inflation continued to heat up in May with headline CPI rising +0.5%, pushing the year-over-year pace to +4.2%, its highest level since 2023. As expected, energy prices were to blame, accounting for about 60% of the overall increase. However, there were encouraging signs of moderation as core CPI rose just +0.2% during the month on easing costs for goods and shelter. On a year-over-year basis, the core rate rose in March and April before reaching a 32-month high of +2.9% in May.

The Fed’s preferred inflation measure, personal consumption expenditures (PCE), followed a similar path, with headline PCE up +0.4% in both April and May, bringing the year-over-year pace to a three-year high of +4.1%. The core PCE annual rate climbed to +3.4%, perhaps even more of a concern given the exclusion of the energy component from the core measure.

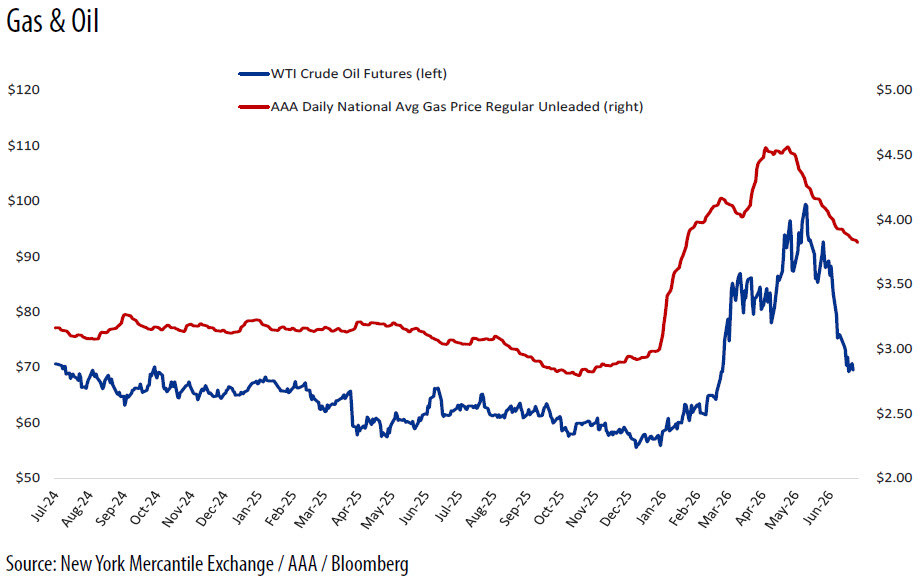

The good news is that energy costs have very likely peaked for the cycle. WTI crude futures reached a high on May 18 with a closing price of $99.47, while the nationwide average price for unleaded gasoline peaked at $4.56 three days later. Crude oil and pump prices retreated significantly in June with WTI closing the quarter below $70 and the average gasoline price at $3.92. The price of oil is now near pre-war levels. Gas prices have been stickier, but the trend is clearly downward. June and July price data should show outright disinflation in the headline with moderating core numbers.

CNBC reported that U.S. oil exports rose to a new record high in April of 5.2 million barrels per day, a 30% increase since the war began. Brazil (+33%) and Venezuela (+43%) also worked to fill the global supply gap, but by the end of June, the International Energy Agency (IEA) estimated “the global oil market likely experienced a net inventory draw of roughly 450–500 million barrels from the onset of the Hormuz disruption through June 2026, making it one of the largest inventory declines in modern oil-market history.” Fortunately, global oil demand fell by an estimated five million barrels per day during the quarter (IEA), or recovery might have been much more challenging.

Lower oil prices will provide near-term relief for consumers, but inflationary pressure has increased in other areas. In a WSJ op-ed last November, Fed Chair Kevin Warsh had written that AI productivity increases would be a “significant disinflationary force.” However, recent indications suggest otherwise. Prices for computer software and accessories rose +15% year-over-year in May, while the soaring price of memory chips is already affecting hardware.

Apple CEO Tim Cook told the WSJ the cost increase was “unlike anything he had seen in any area in over 40 years” while announcing a 15-25% price hike on Mac computers and iPads. An Apple spokesman blamed “rapid expansion of AI data centers, which has created an extraordinary surge in demand for memory and storage.” Data center power demands are also driving consumer energy prices higher. Goldman Sachs has forecasted a 6% annual increase in electricity costs for 2026 and 2027.

Kevin Warsh began his four-year term as Fed chair on May 22. During a formal swearing-in ceremony in the White House, Warsh emphasized the importance of Fed independence, promising that interest rate decisions would not be predetermined at the president’s request. At the ceremony, President Trump actually agreed, claiming that he wanted Warsh to be totally independent. This was a sudden change in tone by the president after months of attacking former Chair Jay Powell for holding rates steady instead of cutting.

As the June 17 FOMC meeting approached, investors were still trying to figure out the new Kevin Warsh. In his previous stint as Fed Governor (2005-2011), Warsh was considered a hawk, willing to sacrifice economic growth in order to hold inflation in check. However, this Trump-selected new version was presumed to be a dove, expected to work in conjunction with administration policies despite holding just one of 12 committee votes. Warsh defied that presumption at his first meeting as chair.

As expected, the FOMC unanimously voted to hold the overnight target range steady at 3.50% to 3.75% for the fourth straight meeting. The official statement was much shorter than usual, but consistent with Warsh’s intent to limit forward guidance.

Three months earlier, the March “dot plot” had indicated a majority of committee members were inclined to cut a quarter point by the end of 2026. At the June meeting, nine of 19 committee members expected a rate hike would be more appropriate this year, given rising inflation expectations. Eight members expected no change and just one called for a 25 basis point reduction. The new chair didn’t submit a forecast.

At his first post-meeting press conference, Warsh began by declaring forward guidance was “not well suited to the current policy conjuncture,” while laying out extensive changes in the committee’s process. The new process will include five task forces in the areas of Fed communications, balance sheet policy, data sources and measurement, productivity and jobs, and the inflation framework. These task forces are expected to be temporary, but there’s no indication of who the “outside experts” will be or how much influence they’ll exert. The clear advantage they’ll provide for a policymaking committee in the process of transitioning …is time.

The only hint of a dovish tendency by Warsh came during the press conference when he said current monetary policy appears to be somewhat restrictive. If anything, Warsh struck a hawkish tone, reiterating several times that the Fed “will deliver price stability.”

As expected, former chair Powell decided to remain on the Board of Governors, allowing him to continue participating in FOMC decisions …at least until he decides the Justice Department probe is “well and truly over.” U.S. Attorney Jeanine Pirro had announced in April that she was closing the criminal investigation of Powell over alleged renovation cost overruns but added the DOJ would “not hesitate to restart a criminal investigation should the facts warrant doing so.”

On a related note, the Supreme Court voted 5-4 in late June to block Trump from firing Fed Governor Lisa Cook for undetermined cause, while a lower court continues to debate whether legal cause exists. Powell had previously said this was “perhaps the most important legal case in the Fed’s 113-year history.” The SCOTUS ruling reinforces Fed independence, limiting the president’s direct involvement in monetary policy decisions for the time being.

After beginning the year with the weakest quarterly performance since 2022, stocks roared back in Q2, logging the best quarter since 2020. The Nasdaq (+12.8%) and S&P 500 (+9.6%) reached fresh highs in early June, while the Dow (+8.9%) closed out the quarter at its highest point on record. Although it seemed counterintuitive to believe stocks would soar amid so much uncertainty, there were several legitimate drivers. Corporate profits continue to grow, up +1.7% for the quarter and +12.8% from a year ago, while 84% of S&P 500 companies beat earnings estimates in Q1. Big tech was once again the primary contributor with microchip demand soaring. The Philadelphia Semiconductor Index (SOX) jumped more than 88% during the second quarter, with eye-popping gains from Micron (+242%), Intel (+216%), and AMD (+186%).

Although de-escalation in the Gulf was a contributing factor to stocks in general, riskier small caps also accrued huge gains with the Russell 2000 surging +21%. But while equity values climbed, gold ( -14.7%) and bitcoin (-13.9%) plunged, failing as (admittedly dubious) inflation hedges.

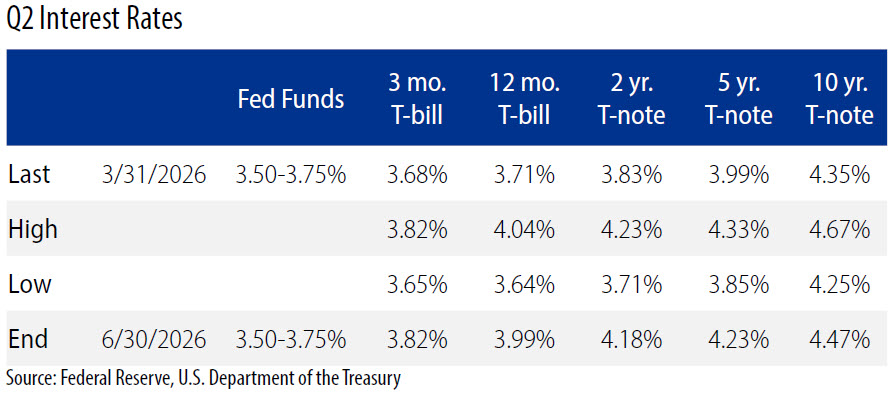

Bond prices fell throughout the quarter, sending Treasury yields sharply higher as expectations for rate cuts morphed into concerns that inflationary pressure would force Fed officials to hike rates.

Although nearly half of the FOMC favored a 2026 rate increase at the June meeting, crude oil prices and inflation concerns have since eased, which suggests Fed officials will have the luxury of waiting to see how the economy evolves in the coming months. The committee’s summary of economic projections (SEP) showed 2026 GDP growth reduced from +2.4% to +2.2%, while the core inflation forecast increased from +2.7% to +3.3%. If the situation in the Middle East remains relatively calm, these tempered expectations could improve in the second half.

The June Bloomberg survey indicated U.S. economists were on a similar page with a median GDP forecast of +2.0% for 2026, and little change in the expected growth rate for 2027. The median inflation forecast showed the annual core PCE rate at +3.2% at year-end, falling to a +2.3% annual pace by the end of next year. Unemployment was expected to hold steady, within one-tenth of the current 4.3% rate through 2027. These same economists expect the Fed to hold rates steady through the first quarter of 2027 before gradually easing by a quarter point in 2027 and again in 2028.

Most economic forecasts assume conflict in the Middle East will end with a peaceful and lasting resolution. Admittedly, this is a big reach as tensions remain high. Although the markets have enjoyed relative calm since Trump announced his memorandum of understanding, several problematic sticking points remain, which suggest the 60-day negotiating window could be extended well beyond the summer.

The new Fed chair is still a wildcard. Trump chose Warsh because he expects Warsh to lobby the committee for lower interest rates, but early indications are that the new chair is fully committed to reducing inflation, which implies a willingness to raise rates. However, just a credible pledge to extinguish price pressure may be enough to jawbone market yields downward while the new task forces take shape.

Unfortunately, the issue of Fed independence is far from over. The president has repeatedly insisted that lower interest rates are the solution to problems ranging from sub-standard GDP growth to “mortgage lock,” and expects rate cuts would fuel future stock market gains. Trump believes replacing Powell and Cook would make for an easier path forward, although any change in monetary policy requires seven of 12 committee member votes.

Treasury yields across the curve declined in June along with crude oil prices, but the bond market ended the quarter signaling at least one rate hike by the December FOMC meeting. That being said, it’s unlikely Fed officials would vote to curtail economic growth in the coming months. The most agreeable Fed policy with inflation moving lower while the economy reestablishes its footing, is a continued pause for the remainder of 2026.

About Scott McIntyre, CFA

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Scott McIntyre specializes in investment management services and is responsible for the management, oversight and trade supervision of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Scott also provides investment advice and consulting, reviews local government investment policies, formulates overall investment strategies, evaluates account performance and oversees the day-to-day operations. He is a member of the Chartered Financial Analyst (CFA) Institute and a CFA Charterholder, a two-term advisor to the GFOA Treasury and Investment Management (TIM) committee, a Registered Investment Advisor, and holds FINRA Series 7, 24, 63, and 65 licenses.

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Scott McIntyre specializes in investment management services and is responsible for the management, oversight and trade supervision of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Scott also provides investment advice and consulting, reviews local government investment policies, formulates overall investment strategies, evaluates account performance and oversees the day-to-day operations. He is a member of the Chartered Financial Analyst (CFA) Institute and a CFA Charterholder, a two-term advisor to the GFOA Treasury and Investment Management (TIM) committee, a Registered Investment Advisor, and holds FINRA Series 7, 24, 63, and 65 licenses.

About Greg Warner, CTP

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Greg Warner specializes in investment management services and is responsible for the management and oversight of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Greg coordinates all client services and portfolio management duties, including security evaluation and portfolio analysis, trading, investment reporting, board presentations, and monitoring of broker-dealer relationships. He is an advisory committee member to the Texas Association of Counties, a member of the Government Treasurers’ Organization of Texas (GTOT), a Registered Investment Advisor, a Certified Treasury Professional (CTP) and holds FINRA Series 7, 63, and 65 licenses.

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Greg Warner specializes in investment management services and is responsible for the management and oversight of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Greg coordinates all client services and portfolio management duties, including security evaluation and portfolio analysis, trading, investment reporting, board presentations, and monitoring of broker-dealer relationships. He is an advisory committee member to the Texas Association of Counties, a member of the Government Treasurers’ Organization of Texas (GTOT), a Registered Investment Advisor, a Certified Treasury Professional (CTP) and holds FINRA Series 7, 63, and 65 licenses.

About Matt Harris, CFA

As HilltopSecurities Asset Management’s Senior Portfolio Advisor, Matt Harris specializes in investment management services for public sector municipal clients. He developed his experience in the banking industry, supporting balance sheet management, interest rate risk analysis, liquidity planning, and investment strategy implementation. At HilltopSecurities, he works closely with clients to develop and implement customized investment strategies, oversees account documentation and reporting, and assists clients with the public funds depository review process, including competitive RFP evaluations. Harris is a member of the CFA Institute and a CFA Charterholder, a Registered Investment Advisor, and holds FINRA Series 7, 63, and 66 licenses.

As HilltopSecurities Asset Management’s Senior Portfolio Advisor, Matt Harris specializes in investment management services for public sector municipal clients. He developed his experience in the banking industry, supporting balance sheet management, interest rate risk analysis, liquidity planning, and investment strategy implementation. At HilltopSecurities, he works closely with clients to develop and implement customized investment strategies, oversees account documentation and reporting, and assists clients with the public funds depository review process, including competitive RFP evaluations. Harris is a member of the CFA Institute and a CFA Charterholder, a Registered Investment Advisor, and holds FINRA Series 7, 63, and 66 licenses.

The paper/commentary was prepared by HilltopSecurities Asset Management (HSAM). It is intended for informational purposes only and does not constitute legal or investment advice, nor is it an offer or a solicitation of an offer to buy or sell any investment or other specific product. Information provided in this paper was obtained from sources that are believed to be reliable; however, it is not guaranteed to be correct, complete, or current, and is not intended to imply or establish standards of care applicable to any attorney or advisor in any particular circumstances. The statements within constitute the views of HTS and/or HSAM as of the date of the document and may differ from the views of other divisions/departments of Hilltop Securities Inc. and its affiliates. In addition, the views are subject to change without notice. This paper represents historical information only and is not an indication of future performance. Sources available upon request.

HilltopSecurities Asset Management is an SEC-registered investment advisor. Hilltop Securities Inc. is a registered broker-dealer, registered investment adviser and municipal advisor firm that does not provide tax or legal advice. HTS and HSAM are wholly owned subsidiaries of Hilltop Holdings, Inc. (NYSE: HTH) located at 717 N. Harwood St., Suite 3400, Dallas, Texas 75201, (214) 859-1800, 833-4HILLTOP.