click below to login to your secure account

By Matt Harris, CFA

Senior Portfolio Advisor

HilltopSecurities Asset Management

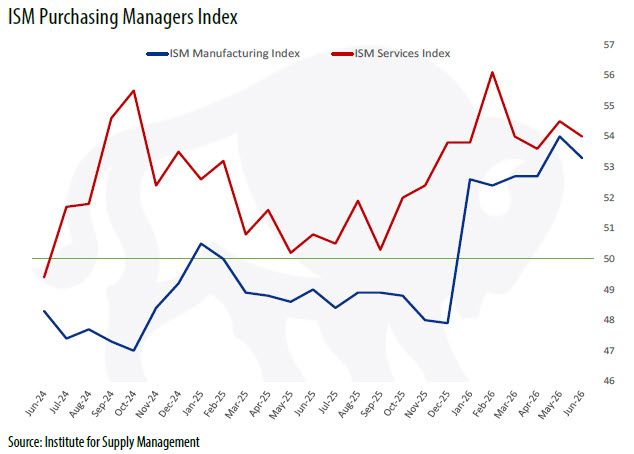

An initial batch of June economic data showed the U.S. economy entering the third quarter on solid ground, although momentum has eased from earlier in the spring. The Institute for Supply Management’s (ISM) monthly surveys of manufacturing and service-sector managers showed composite PMI readings that remained in expansion territory. These surveys are closely watched because they measure whether business activity is expanding or contracting across key sectors of the economy. A reading above 50 indicates expansion, while a reading below 50 indicates contraction. In June, both the manufacturing and services PMIs remained above 50, signaling continued growth, but each expanded at a slower pace than in May.

The manufacturing sector grew for a sixth consecutive month in June, with the ISM Manufacturing PMI registering 53.3, down from 54.0 in May. After several years of uneven performance, the sector appears to have stabilized, with activity continuing to expand, but at a more moderate pace.

One of the more encouraging parts of the manufacturing report was the decline in price pressures. The ISM Prices Index fell sharply from 82.1 in May to 73.0 in June, the largest monthly drop since 2022. Manufacturers had been dealing with cost pressures tied to energy volatility, transportation, supply chain uncertainty, and tariffs. Employment also improved, rising to 49.7 from 48.6, barely missing expansion territory and suggesting manufacturers are moving closer to adding workers again.

The much larger services sector told a similar story. The ISM Services PMI declined to 54.0 from 54.5 in May, still comfortably above the 50 level that separates expansion from contraction. New orders eased to 55.1 but remained solid, while business activity continued to indicate broad growth across the service economy. The employment component improved to 51.2 from 47.9, returning to expansion territory.

Inflation pressures in the services sector also showed improvement, with the prices-paid index declining from 71.3 to 67.7. This is the type of data markets and Fed officials want to see: growth, improved hiring, and less price pressure. However, the level of the prices-paid indexes remains elevated, which means the inflation problem has not yet disappeared.

While both ISM reports were positive on balance, the Atlanta Fed’s GDPNow model offered a note of caution. The model estimate for real GDP growth in the second quarter fell to 1.2% on July 1st, down from 2.5% on June 25th. The decline was driven in part by a lower estimate for real gross private domestic investment growth and a larger drag from net exports.

A 1.2% GDP growth rate would represent slower headline growth, but it does not necessarily point to a weak economy. Domestic demand remains more resilient than the headline figure suggests, with underlying demand reportedly closer to 2.8%. That means part of the slowdown appears tied to GDP categories such as trade and investment rather than a decline in consumer or business activity. That is consistent with the ISM surveys, which continue to show expansion across both major sectors of the economy.

Oil prices have moved back toward pre-crisis levels as the U.S. and Iran continue to work toward a resolution. Ship traffic through the Strait of Hormuz has recovered to roughly 30 to 40 ships per day, well above the worst levels seen during the conflict, though still below the pre-war average of approximately 130 ships per day. OPEC has also begun restoring production that was curtailed during the conflict, and additional supply could come back next month. With oil near $70, lower oil prices should eventually help reduce gasoline prices and broader inflation pressures.

Gas prices have fallen for six consecutive weeks as oil prices have retreated and supply concerns in the Middle East have eased. However, pump prices remain elevated because crude oil is only one component of the price consumers pay. Refining margins, transportation costs, taxes, and other distribution expenses have prevented gasoline prices from falling as quickly as oil prices. Despite those headwinds, lower energy costs should help ease inflation pressures in the months ahead.

For the Fed, the outlook remains complicated. Growth is slowing but not stalling. Employment is growing more slowly. Oil and gasoline prices are moving lower, but inflation remains too high and continues to be the deciding factor for monetary policy. Until policymakers have greater confidence that inflation is moving sustainably lower, the Fed is likely to remain on hold.

The importance of Fed independence was reinforced last week when the Supreme Court ruled that President Trump could not immediately remove Federal Reserve Governor Lisa Cook, allowing her to remain in her position while her legal challenge continues. The Court reached a different conclusion in a companion FTC case, signaling that the Fed occupies a distinct constitutional status among independent agencies. For markets, the Cook ruling is important because it reinforces the Fed’s structural independence at a time when monetary policy is being closely scrutinized.

This week’s FOMC minutes from Kevin Warsh’s first meeting as Chair will offer an early look at how the new Fed leadership is thinking about the path forward. Next week’s June CPI report will be even more important, as a cooler inflation reading could reintroduce the case for eventual policy easing. Meanwhile, President Trump heads to Turkey this week for the NATO summit, where continued progress on Ukraine and allied defense spending could further support stability, lower energy prices, and reduced inflation pressures in the second half of the year.

About Scott McIntyre, CFA

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Scott McIntyre specializes in investment management services and is responsible for the management, oversight and trade supervision of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Scott also provides investment advice and consulting, reviews local government investment policies, formulates overall investment strategies, evaluates account performance and oversees the day-to-day operations. He is a member of the Chartered Financial Analyst (CFA) Institute and a CFA Charterholder, a two-term advisor to the GFOA Treasury and Investment Management (TIM) committee, a Registered Investment Advisor, and holds FINRA Series 7, 24, 63, and 65 licenses.

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Scott McIntyre specializes in investment management services and is responsible for the management, oversight and trade supervision of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Scott also provides investment advice and consulting, reviews local government investment policies, formulates overall investment strategies, evaluates account performance and oversees the day-to-day operations. He is a member of the Chartered Financial Analyst (CFA) Institute and a CFA Charterholder, a two-term advisor to the GFOA Treasury and Investment Management (TIM) committee, a Registered Investment Advisor, and holds FINRA Series 7, 24, 63, and 65 licenses.

About Greg Warner, CTP

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Greg Warner specializes in investment management services and is responsible for the management and oversight of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Greg coordinates all client services and portfolio management duties, including security evaluation and portfolio analysis, trading, investment reporting, board presentations, and monitoring of broker-dealer relationships. He is an advisory committee member to the Texas Association of Counties, a member of the Government Treasurers’ Organization of Texas (GTOT), a Registered Investment Advisor, a Certified Treasury Professional (CTP) and holds FINRA Series 7, 63, and 65 licenses.

As HilltopSecurities Asset Management’s Co-Head of Investment Management, Greg Warner specializes in investment management services and is responsible for the management and oversight of more than $30 billion in institutional fixed income assets for HilltopSecurities’ public sector municipal clients. Greg coordinates all client services and portfolio management duties, including security evaluation and portfolio analysis, trading, investment reporting, board presentations, and monitoring of broker-dealer relationships. He is an advisory committee member to the Texas Association of Counties, a member of the Government Treasurers’ Organization of Texas (GTOT), a Registered Investment Advisor, a Certified Treasury Professional (CTP) and holds FINRA Series 7, 63, and 65 licenses.

About Matt Harris, CFA

As HilltopSecurities Asset Management’s Senior Portfolio Advisor, Matt Harris specializes in investment management services for public sector municipal clients. He developed his experience in the banking industry, supporting balance sheet management, interest rate risk analysis, liquidity planning, and investment strategy implementation. At HilltopSecurities, he works closely with clients to develop and implement customized investment strategies, oversees account documentation and reporting, and assists clients with the public funds depository review process, including competitive RFP evaluations. Harris is a member of the CFA Institute and a CFA Charterholder, a Registered Investment Advisor, and holds FINRA Series 7, 63, and 66 licenses.

As HilltopSecurities Asset Management’s Senior Portfolio Advisor, Matt Harris specializes in investment management services for public sector municipal clients. He developed his experience in the banking industry, supporting balance sheet management, interest rate risk analysis, liquidity planning, and investment strategy implementation. At HilltopSecurities, he works closely with clients to develop and implement customized investment strategies, oversees account documentation and reporting, and assists clients with the public funds depository review process, including competitive RFP evaluations. Harris is a member of the CFA Institute and a CFA Charterholder, a Registered Investment Advisor, and holds FINRA Series 7, 63, and 66 licenses.

The paper/commentary was prepared by HilltopSecurities Asset Management (HSAM). It is intended for informational purposes only and does not constitute legal or investment advice, nor is it an offer or a solicitation of an offer to buy or sell any investment or other specific product. Information provided in this paper was obtained from sources that are believed to be reliable; however, it is not guaranteed to be correct, complete, or current, and is not intended to imply or establish standards of care applicable to any attorney or advisor in any particular circumstances. The statements within constitute the views of HTS and/or HSAM as of the date of the document and may differ from the views of other divisions/departments of Hilltop Securities Inc. and its affiliates. In addition, the views are subject to change without notice. This paper represents historical information only and is not an indication of future performance. Sources available upon request.

HilltopSecurities Asset Management is an SEC-registered investment advisor. Hilltop Securities Inc. is a registered broker-dealer, registered investment adviser and municipal advisor firm that does not provide tax or legal advice. HTS and HSAM are wholly owned subsidiaries of Hilltop Holdings, Inc. (NYSE: HTH) located at 717 N. Harwood St., Suite 3400, Dallas, Texas 75201, (214) 859-1800, 833-4HILLTOP.