click below to login to your secure account

By Tom Kozlik

Head of Public Policy and Municipal Strategy

Hilltop Securities Inc.

It is FOMC week again. The Federal Open Market Committee meets April 28–29, and we expect the policy statement and target rate decision on Wednesday, April 29. This could be Chair Jerome Powell’s final meeting, given the timing around the Fed leadership transition.

We do not expect the Fed to lower its target rate this week. At the last meeting on March 18, the Fed held the target federal funds rate unchanged in a range of 3.50%–3.75%. This week, fixed-income investors can focus less on the statement and press conference and more on the fact that municipal yields remain attractive, especially where long-end municipal-to-Treasury ratios (M/T ratios) remain unusually compelling. We are also expecting information in another area. Five of the “Magnificent Seven” tech companies also report earnings this week. Those results can still move equity markets and, by extension, fixed-income yields.

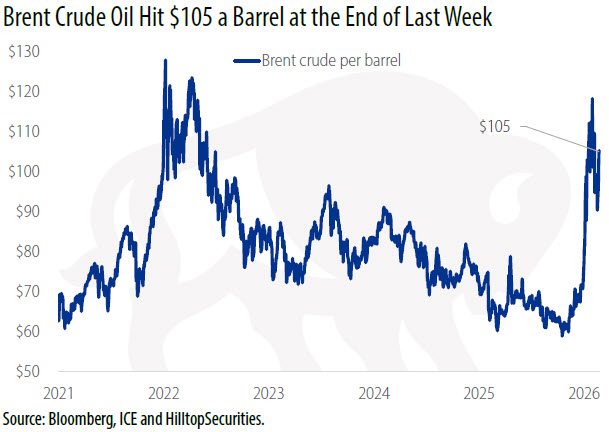

President Donald Trump canceled the planned Pakistan trip for special envoy Steve Witkoff and Jared Kushner on Saturday, pulling back from what the White House had signaled a day earlier as a potential path to restart talks with Iran. This weekend’s backpedaling reinforces how U.S.–Iran diplomacy, the Strait of Hormuz, and shipping risk are still driving the near-term inflation narrative. The price of oil rose throughout last week, and Brent crude settled at about $105 per barrel on Friday, capping a sharp weekly increase as traders weighed supply disruption against the uncertain prospects for negotiations. The President’s social media posture and the ongoing blockade have made trust and negotiations difficult, which keeps an energy risk premium in play even as markets want to move on.

A separate but potentially even more important development on Friday could matter more for longer-run market stability and could also help create a path to lower rates. U.S. Attorney for the District of Columbia Jeanine Pirro said on “X” that she was closing the Justice Department’s probe into Federal Reserve Chair Jerome Powell over alleged cost overruns in the Federal Reserve headquarters renovation, and that the Fed’s Inspector General will continue the review. That move removed an immediate political overhang on the Fed and, in practice, clears the path for Kevin Warsh’s nomination as Fed Chair to move forward. On Sunday, Senator Thom Tillis said he will support Kevin Warsh’s confirmation now that the Justice Department’s investigation is closed. That likely puts Warsh on track for a Senate Banking Committee vote on Wed. April 29 and moves the confirmation timeline to weeks.

For investors looking for a lower rate path over time, this development points in that direction. HilltopSecurities’ Scott McIntyre wrote Friday: “Powell’s now likely departure should assure a more dovish governor will be appointed in his place, increasing the odds of future rate cuts.”

This is a week to slow down and consider the actual numbers available in the municipal market. Absolute yields and long-end ratios are continuing to give investors a better entry point than they have had in a while, and this continues to be an unexpected surprise. If investors are considering adding municipals, the long end is still where they look the best.

Municipal investors added a little over $1 billion to institutional municipal mutual funds for the week ending Wednesday, April 22 per Lipper data. This was a quick reversal of the $427 million outflow experienced the week before. Demand for municipal bonds has been very strong this year. We have seen inflows in 15 of 17 weeks this year, averaging about $1.5 billion per week. Overall, we still expect demand to remain strong amid macro and geopolitical uncertainty.

Some municipal yields ticked up slightly last week, others remained unchanged. The Bloomberg Municipal Bond Index rose about two basis points, closing Friday at a 3.60% yield. It has been encased in a 3.58% to 3.62% range since Wednesday, April 8. The 10-year AAA Municipal Market Data (MMD) benchmark yield closed Friday at 2.91%, or 68% M/T ratio. The long end remains the better story. The 30-year AAA MMD benchmark yield closed Friday at 4.27%, or an 87% M/T ratio, roughly unchanged from the Friday before.

Readers may view all of the HilltopSecurities Municipal Commentary here.

![]() As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or tom.kozlik@hilltopsecurities.com.

As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or tom.kozlik@hilltopsecurities.com.

The paper/commentary was prepared by HilltopSecurities (HTS). It is intended for informational purposes only and does not constitute legal or investment advice, nor is it an offer or a solicitation of an offer to buy or sell any investment or other specific product. Information provided in this paper was obtained from sources that are believed to be reliable; however, it is not guaranteed to be correct, complete, or current, and is not intended to imply or establish standards of care applicable to any attorney or advisor in any particular circumstances. The statements within constitute the views of HTS Public Finance as of the date of the document and may differ from the views of other divisions/departments of Hilltop Securities Inc. In addition, the views are subject to change without notice. This paper represents historical information only and is not an indication of future performance. This material has not been prepared in accordance with the guidelines or requirements to promote investment research, it is not a research report and is not intended as such. Sources available upon request.

Hilltop Securities Inc. is a registered broker-dealer, registered investment adviser and municipal advisor firm that does not provide tax or legal advice. HTS is a wholly owned subsidiary of Hilltop Holdings, Inc. (NYSE: HTH) located at 717 N. Harwood St., Suite 3400, Dallas, Texas 75201, (214) 859-1800, 833-4HILLTOP.