click below to login to your secure account

By Tom Kozlik

Head of Public Policy and Municipal Strategy

Hilltop Securities Inc.

A $428 million weekly outflow does not materially change the 2026 demand backdrop for U.S. municipal bonds given that nearly $18 billion in investment dollars have already flowed in year-to-date, and municipal-to-Treasury ratios still offer attractive relative value, especially for longer maturities. The near-term question is whether private credit scrutiny, U.S. fiscal credibility concerns, and energy-driven inflation risks push Treasury yields meaningfully higher. If they do, municipals could adjust, but the week of April 20 begins from a position of stable demand and competitive tax-exempt yields, not fragility and concern.

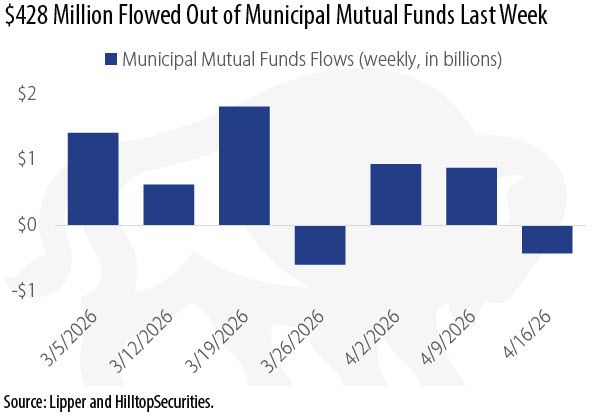

For only the second time in 2026, municipal mutual funds posted a weekly net outflow, with $428 million withdrawn for the week ending April 15, according to Lipper data reported Thursday. We do not see this as the start of a broader demand slowdown. We expect institutional and retail demand to remain stable heading into the next several weeks.

Outflows have appeared in two of the last four weeks, which is a pattern that can show up around tax time. The amounts have been modest relative to the year-to-date picture, with nearly $18 billion flowing into municipal funds so far in 2026. At this point last year, year-to-date flows were barely positive, just under $500 million. The supply and demand balance still favors demand for now, which matters as issuance is likely to remain heavy through the rest of April and into May.

Tax-exempt municipal bond yields held at attractive levels through last week, even with macro headlines developing that have the potential to push Treasury yields even higher.

The Bloomberg Municipal Bond Index finished the week ending April 17 at a 3.59%, about three basis points lower than the week before. The 10-year Municipal Market Data (MMD) AAA benchmark yield ended the week at 2.91% (a 68% municipal-to-Treasury ratio), only four basis points lower compared to Friday April 10th.

Longer maturities of the MMD benchmark curve also slipped slightly. The MMD AAA 20-year and 30-year yields fell three basis points to 3.89% and 4.27%. For investors, the signal is clearest in the long end. Absolute tax-exempt yields remain compelling, and the relative-value case strengthens when you consider municipal-to-Treasury ratios.

The 30-year maturity sits at a still very attractive 87% M/T Ratio, which should move long tax-exempts to the top of the conversation for investors who are not already considering them. The 20-year M/T Ratio, at 80%, remains attractive as well, but it is not offering the same relative value as the longer 30-year maturity.

We are seeing concerns about private credit continue to rise, driven by a mix of complexity, concern about valuations, and anxiety about liquidity that could create pressure if confidence weakens further. HilltopSecurities’ Matt Harris explained, in Growing Private Credit Concerns, that while late-2025 stress and redemption pressure have increased scrutiny, private credit still represents a relatively small share of total debt, and often relies on redemption limits that reduce the odds of forced selling. His conclusion is that the right posture for investors is continued diligence and disciplined monitoring but not panic.

Concerns about the fiscal condition of the U.S. sovereign are increasing from different important sources. First, the International Monetary (IMF) Fund Fiscal Affairs Director Rodrigo Valdes said on Wednesday, “The U.S. needs to reduce its fiscal deficit by about four percentage points of GDP from the current level of 7% and needs a robust credible plan to do so.”

A related concern voiced last week was from Hank Paulson, the former U.S. Treasury Secretary under George W. Bush, who warned during a Wall St Week interview about the risk of softening demand for U.S. Treasuries and suggested the U.S. devise a plan in the case that demand were to weaken.

Large deficits and rising interest costs could push investors to demand higher yields, tightening financial conditions before any true funding stress appears according to an analysis of G7 government debt by Reuters as well.

An important reason this relationship is key to municipals is that if investors demand higher compensation to fund persistent deficits, Treasury yields could move even higher than where they are now. If that happens, municipals could very well follow. Tax-exempt yields could become even more attractive, and issuers could face a higher cost of capital at the same time supply is heavy.

Since the beginning of March, the escalation in conflict in the Middle East has been an ongoing risk for investors. Specifically, the conflict, and the back-and-forth nature of negotiations have continued to feed uncertainty into energy prices and inflation expectations, which could be another potential pressure point on rates. Republican senators are pushing President Trump to find an off-ramp, with energy prices front and center as the November midterms approach.

The U.S. Energy Secretary acknowledged Sunday that it might not be until 2027 that gas prices fall back below $3 a gallon, during an interview with CNN’s Jake Tapper.

This remains an important macro-story and theme to watch for municipals. Energy-driven inflation pressure can keep Treasury yields higher and further complicate the Federal Reserve’s path at the end of April and for the rest of 2026. At the same time, municipals are sitting with still-attractive tax-exempt yields and strong year-to-date fund inflows, which is why the market can absorb a minor weekly outflow without municipal bond demand breaking.

Readers may view all of the HilltopSecurities Municipal Commentary here.

![]() As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or tom.kozlik@hilltopsecurities.com.

As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or tom.kozlik@hilltopsecurities.com.

The paper/commentary was prepared by HilltopSecurities (HTS). It is intended for informational purposes only and does not constitute legal or investment advice, nor is it an offer or a solicitation of an offer to buy or sell any investment or other specific product. Information provided in this paper was obtained from sources that are believed to be reliable; however, it is not guaranteed to be correct, complete, or current, and is not intended to imply or establish standards of care applicable to any attorney or advisor in any particular circumstances. The statements within constitute the views of HTS Public Finance as of the date of the document and may differ from the views of other divisions/departments of Hilltop Securities Inc. In addition, the views are subject to change without notice. This paper represents historical information only and is not an indication of future performance. This material has not been prepared in accordance with the guidelines or requirements to promote investment research, it is not a research report and is not intended as such. Sources available upon request.

Hilltop Securities Inc. is a registered broker-dealer, registered investment adviser and municipal advisor firm that does not provide tax or legal advice. HTS is a wholly owned subsidiary of Hilltop Holdings, Inc. (NYSE: HTH) located at 717 N. Harwood St., Suite 3400, Dallas, Texas 75201, (214) 859-1800, 833-4HILLTOP.