click below to login to your secure account

By Tom Kozlik

Head of Public Policy and Municipal Strategy

Hilltop Securities Inc.

U.S. GDP growth rebounded in the first quarter, and the headline first looked soft, but the make-up of the data is better than the headline number first appears. The drag of the conflict in the Middle East may be starting to impact the economy as well.

The first quarter 2026 GDP advance estimate came in at 2.0% annualized rate last week, according to the U.S. Bureau of Economic Analysis. This result was below the 2.3% consensus expectation, but 2.0% was a welcome recovery compared to the tepid 0.5% growth rate the U.S. economy saw in the fourth quarter of 2025. The 2.0% number still may seem slightly weak at first glance, but there is more strength in the details. Business investment grew 10.4%, and the results were dominated by artificial intelligence (AI) infrastructure and adjacent technology spending. Consumers have pulled back, however.

The economy is continuing to expand. The municipal credit consideration is important here, especially as credit continues to normalize. Public finance upgrades outpaced downgrades in 2025, but the ratio of upgrades to downgrades is normalizing. This is a trend that is likely to continue in 2026. We outline weakness in sectors like K-12 schools, and higher education in February’s The Municipal Market in 2026, HilltopSecurities’ Sector Credit Outlooks. The current U.S. economic engine could be concentrated in only narrow corridors of the country. The economy overall is expanding but this may not be the broad-based country-wide growth of past cycles, where tax bases were lifted across many regions and industries together.

The Strait of Hormuz remains closed. Iran talks have stalled. Operation Project Freedom is now underway. The President informed Congress last week that hostilities have ended under the 60-day War Powers requirement, but the closure of the strait is the market-relevant item, not the stated cessation of military activity. Rising oil prices and sticky inflation do not describe the conditions of a Fed that is likely to cut its target rate.

The direction of monetary policy has become harder to handicap, and the range of plausible rate paths is widening. The complication is not just the war in the Middle East, but also deglobalization through tariffs and trade restrictions, tighter immigration policy, and the approaching transition into the Kevin Warsh Fed era.

Kevin Warsh is expected to be confirmed by the Senate soon, and the Fed under Warsh is unlikely to resemble the Fed under Powell. Warsh has been openly skeptical of forward guidance. He has signaled a bias toward lower rates and has argued that AI-driven productivity gains could pull inflation down structurally, which could justify easier monetary policy rather than tighter. Warsh also will likely want to shrink the balance sheet. Each of those preferences would mark a break from Powell. In addition, Warsh’s Fed could be tested early, and the testing ground is likely going to be the multi-month impact of a closed Strait of Hormuz.

The fiscal deteriorating backdrop of the U.S. is an increasingly important consideration. Data released by the Bureau of Economic Analysis last week showed that the national debt held by the public reached $31 trillion. Therefore, the U.S. debt to GDP ratio hit 100%, for the first time since just after World War II. This is an indicator for potential higher, not lower rates ahead. The deficit is not a cyclical problem the Fed can solve. It is a structural cost the bond market may have to consider and somehow absorb. And, we have heard plenty of recent warnings. Last week Jamie Dimon added to that chorus.

President Trump announced Sunday “Project Freedom, a plan to “free up their Ships, which are locked up in the Strait of Hormuz…” in a Truth Social post. The plan would go into effect “…Monday morning, Middle East time,” according to the President. U.S. Central Command announced on Sunday in a press release, “U.S. military support to Project Freedom will include guided-missile destroyers, over 100 land and sea-based aircraft, multi-domain unmanned platforms, and 15,000 service members.” Project Freedom likely creates more questions than it answers, and creates another element of concern to be aware of since operations escalated in the Middle East several weeks ago.

Municipal yields rose last week on mostly geo-political concerns. The Bloomberg Municipal Bond Index rose about eight basis points, ending the week at a 3.68% yield. The 10-year AAA Municipal Market Data (MMD) yield rose seven basis points ending the week at 2.98% and the 30-year AAA MMD benchmark yield only rose six basis points ending the week at 4.33%, with a still attractive 87% Municipal to Treasury Ratio. Demand for municipal bonds remained stable as Lipper reported another $615 million flowed into municipal mutual funds.

April nonfarm payrolls will be reported Friday morning. That number and the details behind it will go a long way to denying, confirming or redirecting the market from here.

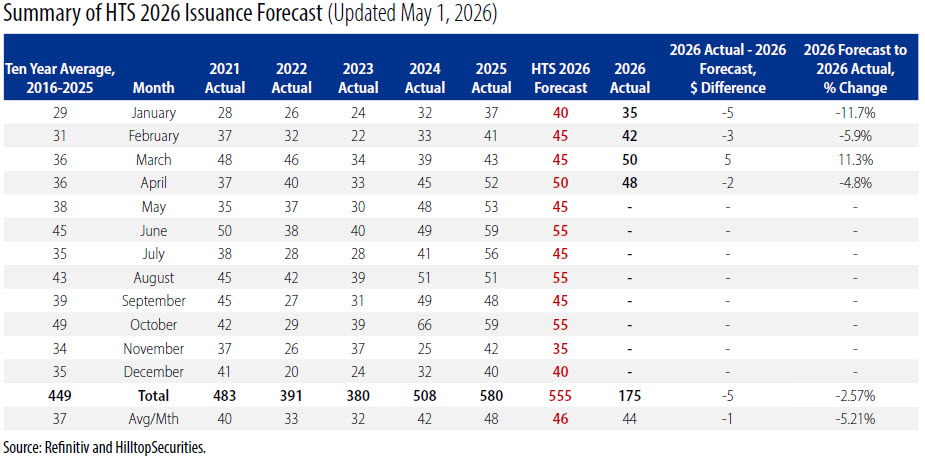

The U.S. municipal bond market has been a major force behind U.S. infrastructure gains this decade, and that impact will likely continue in 2026. Primary market municipal issuance set records, or came close, in four of the last six years. The most recent record was 2025, when public entities sold $580 billion of tax-exempt and taxable bonds. Early in 2025, the American Society of Civil Engineers (ASCE) raised its 2025 infrastructure report card grade to a “C,” from a “C-,” and noted municipal bonds as a key contributor. The ASCE’s infrastructure report card grade is issued once every four years.

Many municipal bond issuance forecasts for 2026 called for another record. Our $555 billion forecast, by contrast, assumed a move toward stability. We expected another year of strong issuance, but not another record year. We wrote that slowing economic growth and fiscal discipline would define municipal market activity in 2026, not acceleration. Another new issuance record would have required broad-based growth above 2025’s level, refinancing-friendly rates, and a stronger credit backdrop than we were expecting.

Based most importantly on results we have observed over the first four months of the year, economic conditions and issuance activity are tracking the path we laid out. Therefore, we continue to expect issuance is likely to come in at about $555 billion for 2026.

Our issuance forecast is not anchored in the level of infrastructure need. It is anchored closer to themes related to economic conditions, financing capacity and the cost of capital. A major binding constraint is whether issuers can borrow at agreeable levels and in a stable credit environment, with enough revenue growth to cover ongoing expenses. That framework aligns with our view that public entities are still working to regain fiscal balance in the Post Golden Age Realignment. For the first four months of 2026 we saw $175 billion of issuance, about $5 billion below our expectation, and $3 billion ahead of what we saw in the first four months of 2025.

Issuance is not running soft, however. It is running close to where we anticipated it would be because the market is moving from a pull-forward surge to a steadier, stable baseline. We do expect issuance to rise to an average of about $50 billion a month or so by November, but then we still expect issuance to ease in the last two months of the year.

We think 2025 results were supported by issuers pulling deals forward to escape perceived threats to the federal tax-exemption. This is likely what created the $55 billion average of issuance from June through October of last year. This explanation points to a potential reset, not a collapse of issuance. Activity is and will remain strong. We expect issuance will settle into a stable baseline above the 2024 mark of $508 billion and likely short of the expectations of $600 billion or higher. The early results over the first four months of this year are consistent with this thesis.

Issuance through April confirms the path toward stability we described in November. We still expect the total annual amount will be strong by historical standards but is likely to fall short of the 2025 record. It will most likely land close to the number we forecast. More importantly the work that issuance funds will continue to produce real infrastructure improvement year-by-year, which is how the improved ASCE infrastructure report grade was earned. Our case for stability is not a case for stagnation or infrastructure avoidance. It is a case for stable, programmatic discipline that turns borrowing into durable infrastructure while keeping debt service, reserves, and ratings pressure in balance, and preserving credit quality and future borrowing capacity.

Four months into 2026, stability is the story. The issuance pattern is steady and consistent with a disciplined year of normalization. The question now is whether the monthly pace builds into October, then slows in November and December in the usual seasonal pattern, while remaining consistent with issuers’ financing capacity.

Readers may view all of the HilltopSecurities Municipal Commentary here.

![]() As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or tom.kozlik@hilltopsecurities.com.

As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or tom.kozlik@hilltopsecurities.com.

The paper/commentary was prepared by HilltopSecurities (HTS). It is intended for informational purposes only and does not constitute legal or investment advice, nor is it an offer or a solicitation of an offer to buy or sell any investment or other specific product. Information provided in this paper was obtained from sources that are believed to be reliable; however, it is not guaranteed to be correct, complete, or current, and is not intended to imply or establish standards of care applicable to any attorney or advisor in any particular circumstances. The statements within constitute the views of HTS Public Finance as of the date of the document and may differ from the views of other divisions/departments of Hilltop Securities Inc. In addition, the views are subject to change without notice. This paper represents historical information only and is not an indication of future performance. This material has not been prepared in accordance with the guidelines or requirements to promote investment research, it is not a research report and is not intended as such. Sources available upon request.

Hilltop Securities Inc. is a registered broker-dealer, registered investment adviser and municipal advisor firm that does not provide tax or legal advice. HTS is a wholly owned subsidiary of Hilltop Holdings, Inc. (NYSE: HTH) located at 717 N. Harwood St., Suite 3400, Dallas, Texas 75201, (214) 859-1800, 833-4HILLTOP.