click below to login to your secure account

By Tom Kozlik

Head of Public Policy and Municipal Strategy

Hilltop Securities Inc.

There is not an imminent threat to the municipal bond tax-exemption right now.

The current backdrop is almost worse because the threat continues to build without

concentrating on one obvious point. The threat is building quantitatively in the form

of fiscal pressure and deterioration. It is building qualitatively, in uneven political

understanding, partial support, and a system where dysfunction makes it easier to ignore the reality rather than deal with it.

There are roughly six months until the 2026 midterm elections, and about thirty

months until the 2028 presidential election. Those timelines matter. Neither is the most

important number right now for the U.S. municipal bond market or municipal bond

investors as it relates to potential fiscal policy that may help or may completely upend

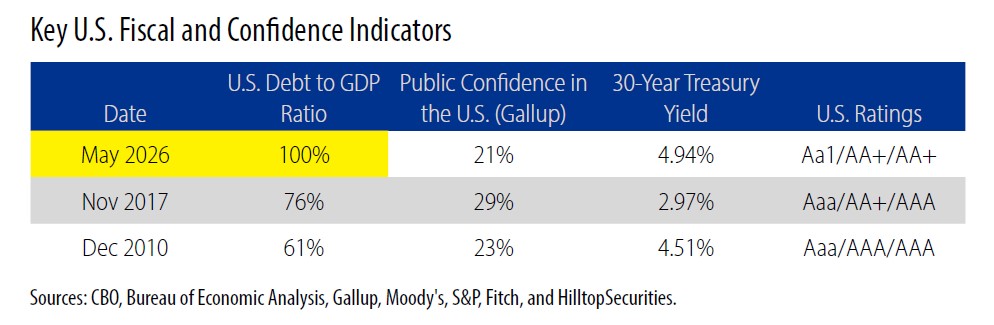

the tax status of the U.S. municipal bond market. The most important numbers right now are not measured in months to an election. They are 100%, 21%, and 4.94%. The decline in the U.S. sovereign ratings is important too.

This is not a moment of crisis like 2009, or 2020. It is, however, a moment of pressure. Even though it is not treated like it is. Taken together, these figures describe an environment defined by constraint rather than choice.

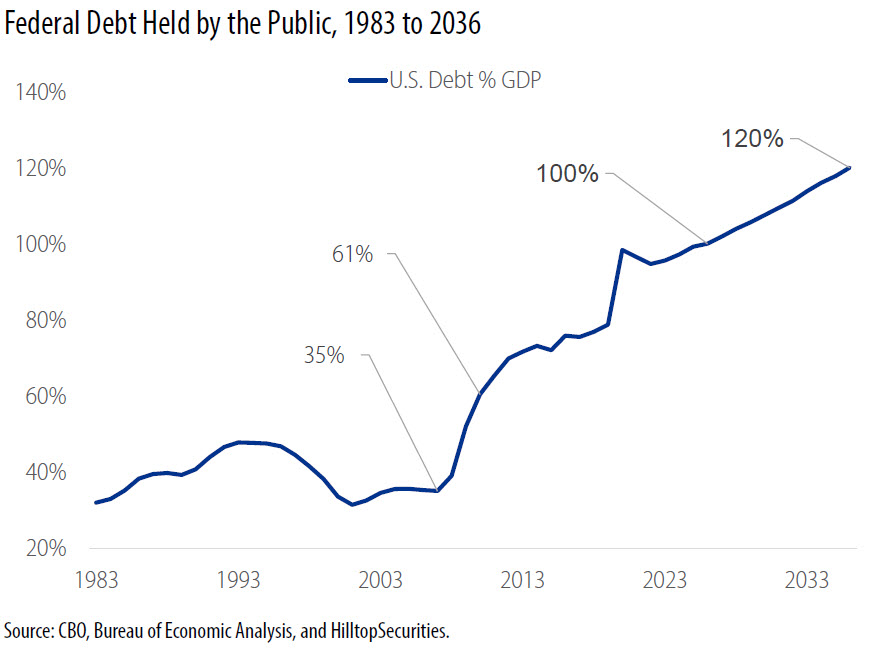

Federal debt above 100% of GDP limits fiscal flexibility. When debt reaches the size of the economy itself, fiscal weakness stops being an abstraction and starts operating as a constraint. A decade ago, U.S. fiscal weakness could be debated as a future risk. At 100% debt to GDP, it has crossed into the present tense. Most importantly from a policy perspective, the menu of easy options to manage the deficit shrinks, and almost any significant proposal shows up with a meaningful price tag and a search for pay-fors.

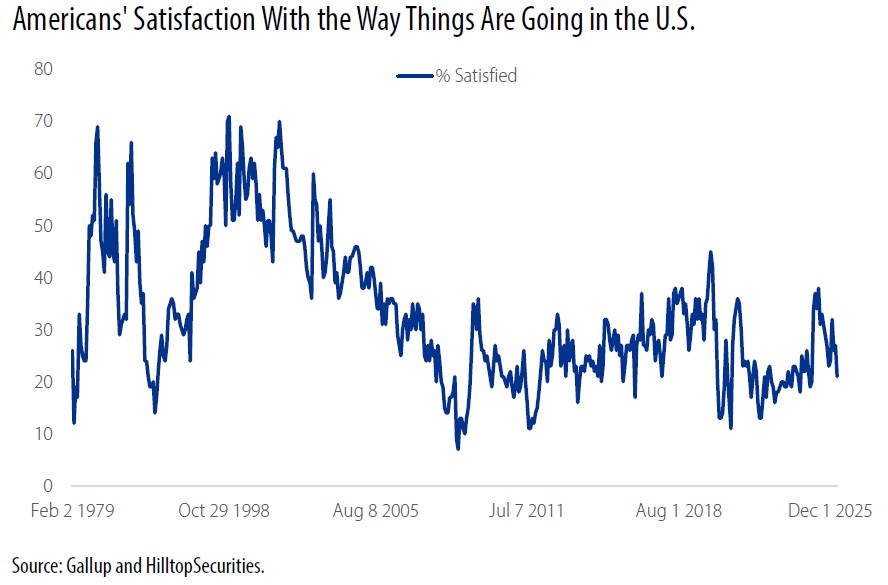

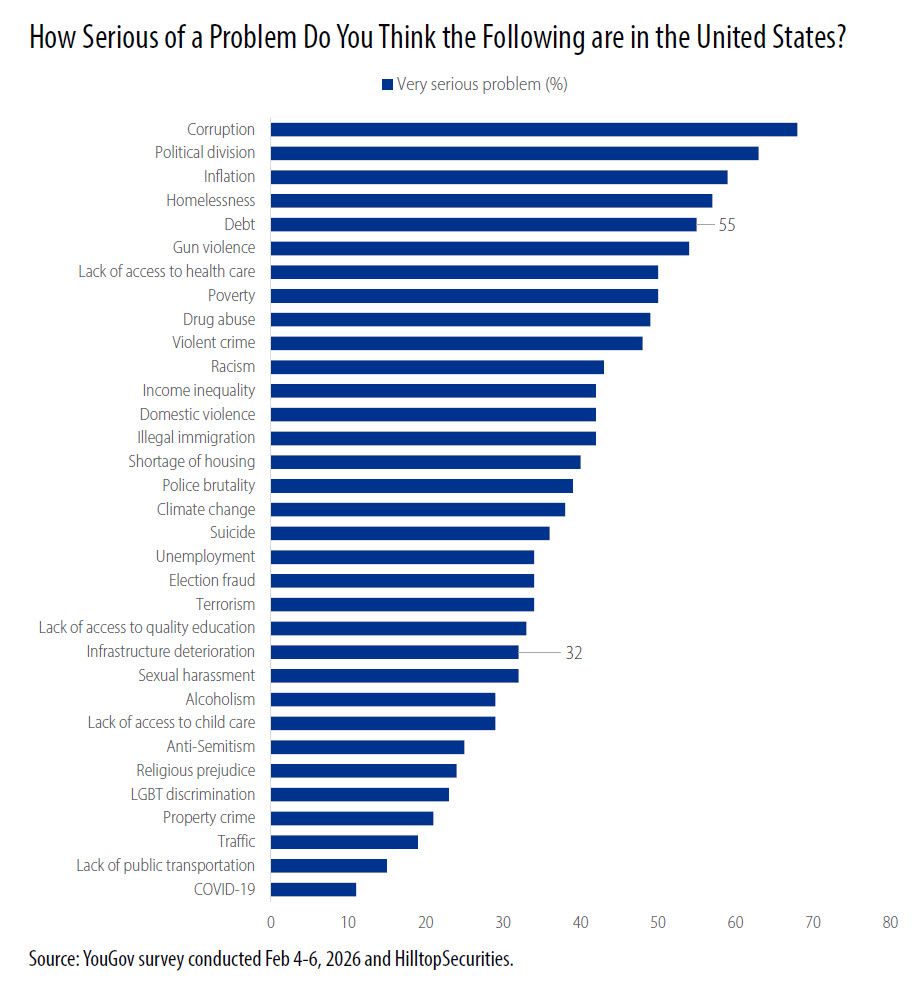

Low public confidence weakens the political foundation that has traditionally protected the tax-exemption. Americans’ satisfaction with the way things are going in the U.S. are near a historical low according to an April 2026 Gallup poll. When public confidence is low, the political durability of longstanding tax preferences becomes harder to assume. When voters are dissatisfied and deficits are large, targeted tax benefits face greater scrutiny as policymakers search for visible pay‑fors. In an environment such as this, policymakers could gravitate toward the easiest pay-fors, and both policymakers and voters are more willing to walk away from policies they do not fully understand.

The current interest rate environment is not a primary fiscal threat, but it is an important signal to monitor. Interest rates are not the core problem, but they amplify vulnerability if investor confidence wavers. The risk is less about today’s rate levels and more about how Treasury investors respond under stress, or uncertainty. Long-term interest rates near 5% can turn borrowing into a compounding budget problem through higher interest expense, however if the deficits are not managed.

The sovereign rating deterioration matters because it captures, especially for readers who follow credit, the direction of U.S. fiscal momentum. Even in 2010, with a unanimous triple‑A sovereign rating the municipal bond tax-exemption was NOT insulated from fiscal debate. The Bowles‑Simpson Commission recommended eliminating all tax expenditures, including the tax-exemption. By 2011, the S&P downgrade marked an early acknowledgment that fiscal strength was eroding and political risk was increasing. Public finance lost the ability to use tax-exempt bonds for advance refundings in 2017. That happened when Washington was still operating with stronger credit optics than it has today, when the U.S. was still rated Aaa/AA+/AAA. Today, with debt near 100% of GDP and all ratings below the highest triple-A standard, the combined erosion matters more, increasing the risk the municipal bond tax-exemption is evaluated as a revenue trade‑off rather than assumed as durable fiscal infrastructure funding tool.

Again, this is not 2009 or 2020. It is not a sudden economic crisis. But still the country’s fiscal position is experiencing sustained pressure. That pressure is largely self-inflicted, which makes it politically tempting to treat long-standing provisions as negotiable. Sustained pressure is where traditional policies like the municipal bond tax-exemption can lose priority to something else if the case for it is not kept front and center.

The municipal bond tax-exemption is not a significant line item in the federal budget, it is not even the largest tax-expenditure. But it is a tax expenditure, and it is large enough to get pulled into negotiations when lawmakers go looking for pay-fors. That is how it ends up in the line of fire, especially when so many issues are grabbing attention.

The key advantage is that it is an important infrastructure funding tool. It lowers

financing costs for infrastructure across the country, and it gives investors a conservative instrument with a tax incentive. A direct attack is probably the least likely path. Most lawmakers will not strike at infrastructure head-on.

The bigger risk is that the tax-exemption gets treated as a negotiating chip in a fiscal deal that is not “about” public finance at all. Or, that it is just thrown onto the negotiating table because it falls into the tax-expenditure category.

That is where intellectual complacency and mythmaking becomes dangerous. People inside public finance know the importance of the tax-exemption and what it does. Some lawmakers and staffers understand also, but many lawmakers and staffers do not. Staff turnover is constant, which weakens institutional memory. When the policy is technical, and the argument for it is not in the room, the policy is easy to misunderstand, and then easy to not defend. That is why lawmakers need regular, plain-language education and advocacy on what the tax-exemption does and who it serves.

After the Great Recession, the push for deficit reduction pulled the tax-exemption into policy discussions that had everything to do with the rising deficit coming off emergency government spending related to the most recent financial crisis. The quantitative and qualitative factors were similar. The circumstances were slightly different. The pressure and the policy goal of government at that time was focused. Advisors to policymakers were looking to cut spending however they could.

The Bowles Simpson Commission published its The Moment of Truth report in December 2010. Its framework leaned on base broadening and proposed to eliminate tax expenditures, including the municipal bond tax-exemption. That is why I treat a severe threat or elimination as a baseline template any time Washington returns to deficit reduction.

In pressured environments, Washington rarely starts with new ideas. It reaches for old ideas that can be pulled off the shelf, scored and reused. These old or longstanding ideas can move from the back burner to foundational architecture. It is my concern that this is what could happen with the Bowles Simpson Commission’s proposal that lawmakers automatically use it, or something like it, as their base case for deficit reduction.

It is not lost on me that this should not even be close to an issue. Tax-exempt bonds are the primary way state and local governments and other public entities finance infrastructure. The case is strong. That case does not automatically translate into political protection, and it is not self-executing.

Federal lawmakers and their staff need repeated, plain-language education on what the tax-exemption funds and what it saves taxpayers. Municipal issuance has been heavy this decade, with record or near record supply in four of the last six years, including $580 billion of tax exempt and taxable issuance in 2025.

The public case is also reinforced by third-party evidence. The American Society of Civil Engineers (ASCE) raised the overall U.S. infrastructure grade to a “C” in 2025 from a “C-” in 2021 and still estimates a $3.7 trillion infrastructure gap over the next ten years. That gap alone supports the continued need for a low-cost, repeatable tax-exempt infrastructure financing mechanism.

The next phase adds a new layer. Digital infrastructure, energy capacity, grid resiliency, water systems, ports, and the environment that supports a more power intensive economy will require capital, and resources. Municipal finance is one of the few systems built to deliver that capital repeatedly, across jurisdictions, to large and small entities and across decades. That is the argument at its core, and it has to be made early and often by state and local leaders, market participants, and constituents. Without that education, the tax-exemption remains easy to forget and hard to defend in a sound bite, especially as fiscal pressure rises.

It still surprises me how many people assume the market potentially could get tax-exempt advance refundings back as a routine legislative add on. That view misreads

what happened in 2017, 2021, 2022, and 2025.

Advance refundings were not taken away because Congress suddenly discovered they were unhelpful to issuers. They were taken away because they were a pay-for. The Tax Cuts and Jobs Act of 2017 repealed the exclusion for interest on tax-exempt advance refunding bonds issued after December 31, 2017, and policymakers had long argued that advance refundings created duplicative federal subsidies by allowing two tax advantaged bonds to be outstanding for the same project.

Private activity bonds were also on the table in 2017. They survived, but the episode should be etched into the memories of public finance.

When Washington is under fiscal pressure, municipal bond provisions may not be treated as untouchable. They can be changed with limited policymaker or public blowback.

We are now in a political era where very large fiscal policy packages move through Congress that cost multi trillion-dollar sometimes. Impactful bond-friendly policies did not make it into fiscal policy passed in 2021 or 2022. They also largely did not make it into last year’s reconciliation package. How could we expect acceptance now?

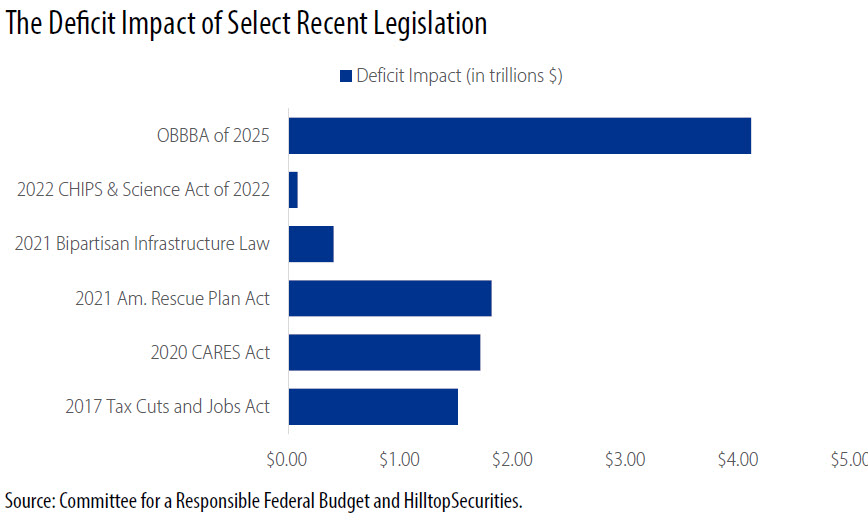

The Committee for a Responsible Federal Government’s analysis, based on CBO data, put the One Big Beautiful Bill Act in the neighborhood of roughly $4 trillion added to the national debt. The takeaway for public finance is not the politics of that bill. The takeaway should be the fiscal signal.

So yes, it matters to keep making the case for reinstating advance refundings and for other sensible public finance tools. The primary job is to defend the foundation. Education and advocacy about the value of the tax-exemption is not optional in this environment. It is risk management, and just plain smart.

Market participants and observers made a mistake heading into the 2017 tax policy negotiations by assuming the tax-exemption was too embedded to be touched. We should not make that mistake again even now when there is not an imminent threat on the horizon. The threat continues to build.

Readers may view all of the HilltopSecurities Municipal Commentary here.

![]() As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or tom.kozlik@hilltopsecurities.com.

As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or tom.kozlik@hilltopsecurities.com.

The paper/commentary was prepared by HilltopSecurities (HTS). It is intended for informational purposes only and does not constitute legal or investment advice, nor is it an offer or a solicitation of an offer to buy or sell any investment or other specific product. Information provided in this paper was obtained from sources that are believed to be reliable; however, it is not guaranteed to be correct, complete, or current, and is not intended to imply or establish standards of care applicable to any attorney or advisor in any particular circumstances. The statements within constitute the views of HTS Public Finance as of the date of the document and may differ from the views of other divisions/departments of Hilltop Securities Inc. In addition, the views are subject to change without notice. This paper represents historical information only and is not an indication of future performance. This material has not been prepared in accordance with the guidelines or requirements to promote investment research, it is not a research report and is not intended as such. Sources available upon request.

Hilltop Securities Inc. is a registered broker-dealer, registered investment adviser and municipal advisor firm that does not provide tax or legal advice. HTS is a wholly owned subsidiary of Hilltop Holdings, Inc. (NYSE: HTH) located at 717 N. Harwood St., Suite 3400, Dallas, Texas 75201, (214) 859-1800, 833-4HILLTOP.