click below to login to your secure account

By Tom Kozlik

Head of Public Policy and Municipal Strategy

Hilltop Securities Inc.

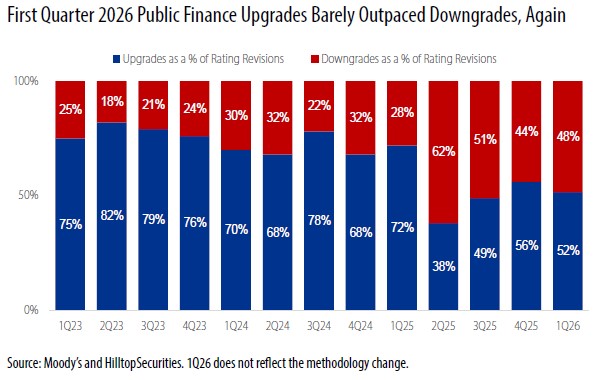

Moody’s first quarter 2026 Public Finance upgrade and downgrade data, released May 15, reinforces that the broad post‑pandemic surge in municipal credit strength remains well behind us. Sector‑level pressures are showing up more consistently in rating actions, with some areas holding steady while others continue to deteriorate.

Continued uncertainty and sector-specific weakening that took hold in the second quarter of 2025, now matters even more for individual investor portfolio construction and positioning. Credit strength is holding in some parts of the U.S. municipal market, but deterioration has continued in others, and the difference is becoming more consequential. For traditional municipal investors, this raises the value of stability and control, which is found in strong triple-A and strong double-A credits that are structurally balanced and carry meaningful reserves.

The importance of credit selection for investors is not a new message, but it is becoming more relevant as 2026 unfolds. After the Great Recession, downgrades outpaced

upgrades for several years and weaker credits were forced to adjust under pressure. The environment today is different, but the lesson is similar. When the tide stops lifting most credits together, investors must know what they own, therefore credit selection and differentiation is important once again.

The results that defined the Golden Age are in the rearview mirror. The Post‑Golden Age Realignment continues, but it is now giving way to a more demanding phase, where support is fading and fiscal pressure is becoming more visible. Credit and rating activity beginning in the second quarter of 2025 through and including the first quarter of 2026 show that improvement is no longer broad based and, in some cases, is no longer occurring at all. Stronger credit outcomes are now isolated and must be earned at the issuer level against a more difficult and uncertain operating and growth reality.

The latest Moody’s public finance rating revisions data (released Friday May 15) confirms that continuation. On the surface, upgrades outnumbered downgrades in early 2026, but that headline is flattered by a one-time methodology change, particularly among special purpose districts. Remove that effect and rating upgrades barely exceeded downgrades at 96 to 90. Rating actions were close to split, with 52% of actions as upgrades and 48% as downgrades, unchanged from 2025 and down meaningfully from 2023 and 2024.

Underneath that surface, credit conditions are weakening in key sectors, especially K‑12 schools and higher education, where cyclical and structural concerns are creating persistent fiscal pressure. Those fiscal pressures are real, not just noise, and they have been and continue to result in rating downgrades. This is also why both the K‑12 school districts and higher education sectors both possessed “Negative” outlooks in our February 2026 The Municipal Market in 2026, HilltopSecurities’ Sector Credit Outlooks in-depth analysis.

The current credit turn started in 2025, and it is still unfolding. U.S. economic growth expectations are less stable than they were a year ago, and the path for GDP is less certain. First quarter 2026 GDP growth rebounded to 2.0%, but the composition matters, with artificial intelligence and tech‑driven activity carrying the expansion. Geopolitics are clouding the inflation and rate outlook heading into the Warsh Fed era, and U.S. fiscal pressure continues to build.

Policy uncertainty has also become constant. The last year and a half have been defined by shifting federal priorities, and there is little clarity on what is likely to come next. Add to that the coming transition in Federal Reserve leadership, which introduces another layer of uncertainty around rate policy, liquidity conditions, and the cost of capital. In such an environment, municipal bond credit quality is no longer insulated. It is very much exposed.

A strong credit profile matters because it tells investors which issuers can absorb stress and keep control of their finances. It also signals the willingness and ability to adjust and maintain fiscal balance under pressure. Strong credits do not rely on favorable conditions to function. They operate on recurring revenues, manage costs early, and preserve flexibility when conditions change.

It is typically the strong triple-A and double-A credits who are more likely to protect structural balance, maintain real reserves, and adjust early rather than after pressure forces the decision. The extra yield from reaching is rarely enough to compensate for the risk of owning the wrong credits when downgrades and spread widening return. Put simply, strong credits do not rely on the cycle to look stable. They remain stable even when the cycle turns.

Readers may view all of the HilltopSecurities Municipal Commentary here.

![]() As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or tom.kozlik@hilltopsecurities.com.

As Head of Public Policy and Municipal Strategy, Tom Kozlik advises HilltopSecurities’ businesses and clients on strategies related to U.S. public policy, public finance, and infrastructure. He publishes regular commentary that provides insight into current trends affecting these themes across a variety of sectors and geographic regions. Kozlik is frequently featured in print, digital, and broadcast news segments and regularly offers his expertise as a keynote speaker and panelist at industry conferences and events across the country. He can be reached at 214.859.9439 or tom.kozlik@hilltopsecurities.com.

The paper/commentary was prepared by HilltopSecurities (HTS). It is intended for informational purposes only and does not constitute legal or investment advice, nor is it an offer or a solicitation of an offer to buy or sell any investment or other specific product. Information provided in this paper was obtained from sources that are believed to be reliable; however, it is not guaranteed to be correct, complete, or current, and is not intended to imply or establish standards of care applicable to any attorney or advisor in any particular circumstances. The statements within constitute the views of HTS Public Finance as of the date of the document and may differ from the views of other divisions/departments of Hilltop Securities Inc. In addition, the views are subject to change without notice. This paper represents historical information only and is not an indication of future performance. This material has not been prepared in accordance with the guidelines or requirements to promote investment research, it is not a research report and is not intended as such. Sources available upon request.

Hilltop Securities Inc. is a registered broker-dealer, registered investment adviser and municipal advisor firm that does not provide tax or legal advice. HTS is a wholly owned subsidiary of Hilltop Holdings, Inc. (NYSE: HTH) located at 717 N. Harwood St., Suite 3400, Dallas, Texas 75201, (214) 859-1800, 833-4HILLTOP.